|

|

PRIDGER |

|

E-Mail |

John Q. Pridger's

|

|

BUY AMERICAN:

http://www.usstuff.com | http://www.madeinusa.org/

| http://www.stillmadeinusa.com/

| http://www.buyamerican.com/ |

|

|

|

PRIDGER |

|

E-Mail |

John Q. Pridger's

|

|

BUY AMERICAN:

http://www.usstuff.com | http://www.madeinusa.org/

| http://www.stillmadeinusa.com/

| http://www.buyamerican.com/ |

|

|

Pridger's Web Host Important Links BLOG FEB-JUL

2010 DEC.

2008 JUL-DEC.

2007 DEC.

2006 |

August 27, 2010 GOD IS WATCHING, BUT WASHINGTON IS FIDDLING Pridger gets many more personal emails than responses to this so-called blog. This is because, while Pridger has relatively few friends, his blog seems to get even viewer readers, and no email response at all. It's apparently almost invisible on the Internet, and Pridger has thus far chosen to keep it that way – for the time being. And the "time being" has already stretched into years. So this isn't an ordinary blog – it's an extraordinarily exclusive weblog of personal opinion essays. The personal emails are seldom about anything that Pridger writes about here. In fact, they are usually the standard "forwards" that are making their unending rounds in cyberspace. But sometimes they provoke answers that qualify for blog post status. One such "forward" hit Pridger's inbox today. It contained a list of oxymoronic questions and statements. Chances are you've received a variation of it yourself more than once. This one came under the heading "Ever feel like your life is an Oxy-moron…. ?" and it featured a graphic of Daffy Duck. One of the questions caught Pridger's eye and he wrote a rather long and typically rambling answer. The question was: If all the world is a stage, where is the audience sitting? Of course, an answer wasn't expected. But the friend got one anyway. And, Pridger's mind working the way it usually does, had to wax religious and political in contemplating the answer. Where would the audience be sitting? Space, of course. And here's some of the rest of the story...

But then Pridger couldn't resist getting off subject, as he quite frequently does.

And that's some of what's transpiring on the world's stage. We can pray that God watching from above will have mercy on our souls, but what the American people need right now is a government that is on their side. Unfortunately, the prospects don't look very promising at the moment. JQP August 25, 2010 WHY AMERICA IS FAILING – ECONOMICS ONE OH! ONE There's a very simple formula that lays it on the line. It's so elementary that it appears far too simple to have any rational application to modern day economic theory. I = P X P That is, Income equals Production times Price. There's nothing simpler, more basic, or demonstrably true than that. It's so elementary and obvious that we miss its significance. But it works for nations as well as corporations and individuals. Production, of course, includes production of basic raw materials (both agricultural, forestry, fisheries, and industrial/mineral), and all of the value-added processing that occurs between initial production and and final consumption. Price, and therefore potential income, increases at every stage along the value-added and wholesale/retail market chain. If you discount price at any stage of production, then, naturally, the incomes of workers involved will be shorted, and ultimately the national income itself is shorted in a multiplying effect. The price an individual or corporation receives for its production is the difference between profit and loss, survival and failure, a good return or a poor return, poverty or prosperity. Where the American economy has failed has been in national economic and trade policies that removed a great deal of production from the national economic equation. When production is reduced, of course, production times price naturally renders a reduced national income. If consumption remains the same, pretty soon it naturally follows that the national income is incapable of supporting the national economy. And that's where America finds itself today. The production that services American consumers, of course, is still going on. But far too much of that production is going on elsewhere. Shifting production to Mexico and China so that business corporations could make a better income, and Wall Street could prosper, might have been good for the corporations, but it also spelled suicide for the national economy economy itself – and must ultimately end in collapse. To keep the consumers happy, and Wall Street cooking, real national income was progressively replaced by debt injections. As production – real wealth production – was being undermined and removed from the national economic equation, credit has been substituted for income, giving the illusion of continued prosperity. But while getting a loan check may appear as income to the unwary, it is clearly and definitely not income. These are simple irrefutable facts, the evidence of which stand out like a multi-trillion dollar gorilla in middle of the room, in the form of increasing budget deficits, national debt, and obscene trade deficits. And this doesn't even address the problem of absolutely artificial, criminal, and toxic economic bubble-activity which has been going on. Those things grossly exacerbated and multiplied the effects of "normal" suicidal economic and trade policy our government has been pursuing for over fifty years. The public has been rightly outraged at financial bailouts for some of the biggest, supposedly richest, men and financial institutions in the country. Such bailouts are actually more criminal than many of the crooks and institutions that were baled out. They have set us many times further behind the economic eight-ball than we were before. The public is pretty aware of this, but the public has not yet been fully appraised of the fundamental problem which remains un-addressed as if it were not a problem at all. Unemployment is high, first and foremost, because domestic production (the real engine of wealth) is low, and it has been getting progressively lower since the advent of free trade and globalism – long before the financial house of card started crumbling. When you build a house on shifting sands, that's bad. But when you build a house of cards on shifting sands, that's even worse. We hear our astute politicians admitting that we need to produce more. But they think we need to produce more for export, so we can balance our trade with the rest of the world. But this is to totally miss the point. In and of itself, trade does not produce a damned thing. It adds no value products. In fact it adds expensive shipping costs! Unless someone is getting cheated, there is no profit in trade. It's a zero sum game. Done on an equitable bases, trade amounts to an even exchange of goods. It makes sense only when they are different goods, where one nation trades raw materials or manufactured goods that it has or produces, for other raw materials and manufactured goods that it doesn't have and can't produce produce for itself. The answer to the trade deficit is not in creating more export jobs, but more jobs that produce for the domestic marketplace – the things we used to produce for ourselves, and still consume, but are now buying from others elsewhere using debt financing to cover the trade deficit. We already trade far too much and produce far too little! We trade or buy manufactured goods that we can produce for ourselves, did produce for ourselves, and should still be producing for ourselves! But our leaders have chosen to uplift the rest of the world at the expense of American workers, with that rationale that slave-like foreign labor is good for the foreign laborers, good for American consumers, and extremely good for multinational corporations and Wall Street. It of course throws our basic equation out of kilter by isolating the producers from the consumers, and co-opting and redirecting price and income away from producers and consumers and into the hands of corporate capital, at great cost to all of the people involved. Globalism is good for international corporations, but very bad for nations and peoples. The proof of this is suddenly becoming apparent even to the untrained eye. Yet the core causes still evade far too many eyes. It is incredible to think that one of the largest continental sized nations in the world, and one of the most liberally endowed nations by any measure, which once was the most productive and prosperous nations in the world, can no longer pay its way in the world! And while it still purports to militarily and economically dominate the world to boot! The tax base in that nation is in decline, while the corporations either continue to prosper or get taxpayer bailouts. The lion's share of the now international income is going to corporations, and bypassing the people and the nations. On behalf of big corporations, debt is socialized and profits remain inviolably privatized. Income = Price X Production still applies, of course, but international capital has overwhelmingly become the prime beneficiary of the system – and international capital is effectively totally divorced from fundamental national interests and the interests of workers and the people at large, no matter what country they may live in. The consumer is still important to the interests of capital, naturally, but the consumer will eventually consume no more than his contracting personal income can cover. When he's lost his income, expended his credit, and lost all, his consumption will be negligible. The government itself brought this nation to its present impasse, yet it's leaders still don't seem to have a clew as to what has gone wrong and why. We have at least 20 million willing workers just waiting for the opportunity to produce. But their jobs have been sent to Mexico, China, and a score of other countries and nobody seems to have a clue as to why they went or to how to get them back. JQP August 24, 2010 OUR MYSTERIOUS PRESIDENT If you've ever wondered how somebody named Barack Hussein Obama could get on a fast-track to becoming the president of the United States, here's some mighty interesting background material. This is not only interesting material on our very mysterious president and his family, but a downright interesting geopolitical history lesson. It's a pretty long article, but well worth the read. Be sure to read all three parts: "Obama: All in the Company," by Wayne Madsen : http://www.opinion-maker.org/2010/08/obama-all-in-the-company-part-i/ JQP August 17, 2010 TRICKLE-UP ECONOMICS If we had a nation with government "of the people, by the people, and for the people," and a real people-driven free market, rather than a Big Brother government devoted to both people control and international corporatism, we'd perhaps be a lot more familiar with trickle-up economic fact than trickle down economic theory. Unfortunately, no great economist or writer that Pridger knows of has yet seen fit to lend the term any kind of public recognition or respect, and it falls to this rank amateur to cobble together some sort of explanation to that end. Trickle-up is not a theory but a known fact of life in a true free market economy in which industrialization, huge government, central banking, financial capital, and mega-corporations have not attained omnipotence in and over all economic affairs. The trickle-up that Pridger will attempt to explain is correlative to what has been formally described as the trickle up effect, but is more comprehensive because it is an economic proposition which includes the requisite that government itself would not only be a fair referee, but to adopt a people-friendly economic philosophy and monetary system.

It's pretty easy for most people to grasp the essential ideas behind trickle down economic theory. As in the brief description above, trickle down not only make senses, but, more to the point, simply appears to be the way things have actually worked throughout the industrial and financial era. Trickle down is sort of a corner of the cornerstone of Keynesian economic's, ideas of deficit spending to stimulate a lagging economy. This, in turn, was the precursor of the idea of literal trickle down – "helicopter money" that the Fed chairman Ben Bernanke recently jokingly suggested (from a quip by Milton Friedman) as an easy means to fight deflation. In the simple terms, expressed in Pridger-speak, trickle down is explained thus:

Trickle down might have worked much better than it did, of course, had all of those money-bagged benefactors not fashioned such deep pockets, big money belts, and offshore banking havens for themselves. But we should have known they inevitably would. Even the Bible told us that the love of money is the root of all evil – meaning, in part, that those who covet money as their life's interest, and who have the most of it, have a very great propensity to hang onto it. Trickle-up economics is much more akin to supply side economics than trickle-down economics – but it is even more closely related to the distributism as advocated by G. K. Chesterton, and at its core sits upon an agrarian foundation as all economies should. A description of trickle-up economics can perhaps be expressed thus:

Thus all wealth starts at ground level and then works it's way up through market chains and trade channels (through refinement, processing, manufacturing, distribution, and consumption, etc.), all accomplished by the hand of human labor. This is the real font and source of wealth creation – the foundations that literally everybody in the world stands upon, and depends upon, for both survival and the capital required for all of the great things that mankind has proven capable of.

Trickle-up economics is about justice and just rewards – and, more specifically, initial just rewards. Unfortunately our society has focused almost entirely on intermediate and last rewards and discounted initial rewards. The rich get first dibs (and thus get richer), and then there is usually some consideration for the middle class. And the unproductive poor are sometimes looked after in advanced societies. However, the poor hard working, and eternally productive, farmer (as important as he has always been), has traditionally been at the bottom of the economic ladder, when he should be the first to be amply rewarded for his valuable and productive labor, whereas many of the richest men in the world are also some of the least productive, if not the most criminal.

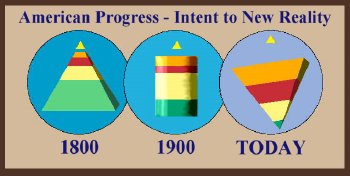

The farmer and the agrarian sector of the economy may be at the bottom of the economic pyramid. But this should not reflect their economic status within the economy. Their importance is obvious in the fact that they constitute the very foundation and base of the economic pyramid – the most important position of all! Undermine that base, and the whole pyramid will collapse. In a just system, the segment of society that comprises that base should be fairly compensated as the font of all initial life-sustaining initial wealth. But today, we've got the whole pyramid askew, and here's one of Pridger's ways of illustrating the transformation of our socioeconomic situation (see below). Today our pyramid is inverted, it's spinning like a top, and beginning to wobble erratically. In the illustration below, the green represents the agrarian base. The light yellow represents the industrial productive sector (both individual free enterprise and productive businesses). The red represents the services sector. The orange represents pure government. The mid-point, given as 1900, is shown in a drum shape – still a stable construct, but reflecting the rise of industrialization predating the ultimate triumph of big government and financial corporatism as we know it today. And, fear not! That little gold triangle above the pyramids and drum doesn't represent the Illuminati, but the steady omnipresence of God. If you tend toward atheism, just pretend that the gold triangle isn't there – the illustration is no less valid.

The rural economy, which is (or once upon a time was!) naturally driven by agricultural production, is the most important first tier of all economic activity, for the entire economy, and all people, depend on it. And the sociopolitical aspects of this are just about as important as the economic aspects. As Thomas Jefferson once opined:

And further:

If Jefferson was right, and cultivators of the earth are the most valuable citizens, then it would naturally be beneficial to the nation to have a significant percentage of the population in that category. But the cultivators of the earth are now vastly outnumbered and outvoted by the mobs of large cities, and stand alone and vulnerable against a great array of powerful commodity traders and financial and economic interests upon which he must depend to extend credit and purchase his production. His products are sold on their terms rather than his own, or even anything that could be called a free market. Today there is a resurgence of small, independent, mostly organic, farmers and "farmers' markets." But they struggle against tremendous odds and the overwhelming handicaps presented by the omnipresence of the corporate marketplace. Today, of course, the "powerful" farm lobby, is really the corporate agribusiness lobby which does not speak for farmers nearly as much as the interests of relatively few powerful agribusiness conglomerates, for the lobby is predominately comprised of commodity trading giants, the big meat packers, corporate food processing and wholesaling giants, large agricultural petro-chemical companies, and proprietary seed combines, etc. The numerically few farmers, who now farm on an industrial scale, are naturally beholden to them and their lobby for sustenance and survival. Unfortunately, feudal society made lowly serfs of the farmer, who labored for the landed gentry which reaped most of the gains of the farmers' labor and harvests. But in the days of meager wants, even fewer luxuries, and sometimes modestly generous nobles, the life of the landless peasant farmer was often not all that bad. Sometimes, under enlightened stewardship, it was modestly prosperous and fulfilling station in life. The life and comforts of the gentry and nobility depended on the the well-being and contentment of their serfs. The farm, whether tended by serfs or in the hands of yeomen farmers, was the root and embryo of capitalist enterprise. The farmers' market was the very first market – the source of community nourishment. Food, fiber, and shelter are the first and life-long requirements of every individual, whether serf, school teacher, banker, lawyer, or king. Everybody has to be fed, clothed, and sheltered throughout their lives, most all of which are dependent on the agrarian base. People must eat before they can do a day's work at any calling. Furthermore, most people have to be fed, clothed, and provided shelter for the first 16 to 25 years of their lives without ever having to seriously turn a hand at making a living. The farm of the humble independent yeoman farmer, especially as they developed in the New World and later the United States, embodied all of the fundamental attributes of a factory – and what a wonderful factory the well run diversified family farm was! The independent farmer came into his own during the history of the United States. It was a uniquely American institution. Always struggling, he reached the epitome of respectability and prosperity during the first century and a half of our national existence. As a general rule, diversified American farms commonly produced two or three staple grains, hay, various meat and work animals (goats, sheep, swine, and cattle, horses, and mules, etc.), poultry, eggs, milk, butter, fruit, and an array of garden vegetables. All were cash crops to one degree or another with perhaps one or two predominating which produced the lion's share of the family's cash income. The American landscape was once filled with such farms, of varying size and degrees of productivity and prosperity. Long before the great era of independent farming came to an end in America in the mid-twentieth century, this nation had become the breadbasket of the world. That era did not come to an end because of food shortages or the inefficiencies of relatively small family farms, but despite their efficiencies, and probably because of their independence. It came to an end because the government itself, all of a sudden, had a "new vision." In a nation whose government had become increasingly enamored with corporate scaled enterprises and the supposed efficiencies of scale as the capitalist model (and influenced by them), there was no room for a large independent farming class. With the big corporate scale enterprises also came the rise of "scientific everything," which in time evolved in a great faith in chemical solutions to everything. Effectively, the American government would challenge the agricultural collectivism of godless communism, with agricultural collectivism under equally godless corporate capitalism! Before the agricultural chemical era, and the advent of proprietary seed production, farmers not only planted, cultivated, and harvested crops, but the crops themselves provided the seeds for the next plantings! It was a miraculous capability uniquely available to the farming profession above all others. That was one of the keys to the farmer's unique degree of independence – and the government and the corporate agribusiness lobby very effectively colluded to put a stop to it! There is no such thing as something for nothing when it comes to wealth creation of course. Labor is always involved. The only instances where something for nothing is apparently possible are when gifts are made, income is coercively redistributed by government, robbery takes place, or when professions like lawyers and bankers exist. Even in these cases something is required even if it is nothing more than shrewd or criminal thinking. But to steer away from the politics of the matter, here is the unique thing about farms and the profession of farmers. Farmers come closer to creating something out of nothing than any other profession or class of people – in bringing forth new wealth from the soil. The truly closest thing to producing wealth from almost nothing is when you plant a single seed, tend it and nurture it into maturity, and harvest a hundred or more such seeds from what was before only one seed. That is a miracle. And other miracles take place on farms under the careful husbandry of farmers. Animals are conceived, born, and grow into market products; baby chicks are hatched from eggs and go on to lay hundreds of eggs. Cows and other animals grow on nothing more than naturally occurring grasses, and produce their own young, which in turn provide meat, milk, butter, and cheeses. Fiber from cotton plant boles (or, heaven forbid – from hemp!) and wool from sheep and other animals provide us with clothing and a host of other products, from rope and paper to sails and tents. Corn, and the amazing soybean not only provide food products, but an incredible array of other products from fuel to ink and plastics. The byproducts of agriculture are beyond categorizing in a short article. These are all miraculous things, and these products in their initial form represent the first and most vital wealth ever produced in this world for all of us. But it takes hard work on the part of farmers who produce all of those agricultural products. This remains true even in the present age of industrial scale farming, except most of the people have been replaced by inhumanly large machines, and the system is no longer as healthy or sustainable as it was under the diversified family farm system. We're beginning to hear that the government has become the largest business in the country. This is patently untrue. Government may command, and tax and spend more money, but agriculture remains the largest business by far – and by far the most important even in today's Wall Street dominated economy. Our agricultural production not only provides this nation with its primary source of nourishment, it also provides it with its primary source of export revenue. Our agricultural export industry is about the only one in which we do not yet suffer a huge foreign trade deficit. It would make a lot more sense if this singularly immense national industry, which literally spans the nation east to west and north to south, once again employed a significant percentage of the people, rather than the mere 2% that it employs today. In our vast agricultural industry, our nations primary source of initial wealth, like money bubbling out of the ground, is being discounted at the source in order to provide big profits to a few large commodity trading corporations and a small army of commodity speculators. Rather than providing some degree of prosperity for twenty-five or thirty million farming families, and a much larger number of local supporting business people, only about 6 million remaining farmers are being supported. And, in spite of their incredibly efficient production record, only government subsidies can keep their heads above water! There's something absolutely wrong with that circumstance! And this brings us back to Trickle-up economics. If there were 25 million farm families scattered all over the country making their living off of the land, their business activities and and incomes would still be supporting the thousands and thousand of diverse farming communities and small towns around the nation, most of which have been emasculated during the last sixty years or so. Most that remain have imploded on themselves, with most locally owned businesses simply disappearing into the sunset. As Charles Walters often pointed out, agriculture is both the "balance wheel and flywheel of the national economy." It's rooted on the very ground that stretches from sea to shining sea. But only when a significant percentage of the population is actively engaged in agriculture, on relatively self-sufficient, sustainable, and self-sustaining farms, can it also be provide a dependable food insurance policy to the nation. A sound "national food insurance policy" is not only a matter relating to insuring that the people always have ready access to food, it's also very much a national security issue. Yet few people, much less our politicians and policy makers in Washington, ever give that a thought. Back on Main Street, as in the case Pridger's home town, many of our once thriving farming towns and communities now exist with no visible means of support! Apparently they survive largely on government largess, welfare and retirement checks, public payrolls, food stamps, unemployment checks, and subsidized housing – supplemented by the payrolls of the full array of corporate fast food restaurants and chains stores whose main contribution is to siphon off much of the community's income as possible and send it to their own financial centers. Under this modern economic model, the real font of wealth creation is staunched at its source. Farming communities, in spite of the riches produced by their surrounding agricultural lands, are no longer self-supporting as they should be. Once vibrant towns and communities all over the nation effectively live on welfare. They are essentially consumptive communities that do not produce anything to contribute to their own survival and well-being – just like most large population centers have have become with the demise of our once great national industrial base. Like the State and federal governments themselves, they are no longer able to earn their own keep in spite of the rich land which they occupy. This circumstance, of course, which was vigorously pursued by economic policies of the government, was to cut the very legs out from under the national economy. Real production has been discounted while consumptive non-production has been made king. Independent farmers, of course, made their own jobs. But as independent as they were, they never had an easy go of it. Starting out usually required incurring debt to bankers, and bankers usually managed to keep them in debt throughout the the whole working lives and succeeding generations. Agricultural wealth production is the closest thing to actual wealth creation, because it literally grows wealth – vital consumable wealth, of a variety that we simply cannot survive without – it grows it out of the very soil, (and in this we include forestry and fisheries, though fisheries are actually in the separate category of hunting, fishing, and gathering). Importantly, agriculture raw materials are infinitely renewable and self-sustaining under proper management. They are powered by the sun and nourished by the earth. Next to agriculture, the closest thing to initial real wealth creation is resource extraction through mining, quarrying, and drilling into the earth. Oil and minerals and stone, like agricultural products, represent new wealth coming into the the economy from the earth. Though they are not renewable resources, and many may not be unlimited, essentially the same economics apply to them as apply to agricultural raw materials. Unlike farming, oil and mineral extraction is more suited to corporately organized undertakings because of the large capital investments required. In spite of this, they represent another major facet of trickle-up economics. Extraction is the first step to a whole vast array of value-added processes which mushroom in value as they make their way up the market chain. The idea that pile of iron ore has the potential to become a brand new car, or any number of other products, seems almost as miraculous as the seed a farmer plants. Harvesting and extracting of raw materials are the initial creation of wealth. Refining, processing, fabrication, building, manufacturing, transportation, and final sale and consumption flow from the ground up – each stage of value-added processing dependent on the former stage – it's all real wealth trickling up and increasing in value as it does so. Money is the representative of wealth, and labor is what produces wealth. So, if there is to be justice in any economic system, and a degree of prosperity among the laboring classes, it is important that the initial producers are justly compensated for their work. Miners, oil workers, steel workers, and workers in corporate industry in general are generally well compensated. Farmers have usually been the one man out that seldom get a fair price from the products of their labor, yet theirs are the most important production of all! During our short era of enlightened farm policy with parity pricing for farmers, during World War Two and a few years thereafter, it was calculated that for every farm dollar earned, the value-adding "trade turn" produced seven additional dollars of national income to the farm dollar. Shortchanging the farmer – the biggest producer of all – has a ripple effect right up through the entire market chain, depriving the economy of income. In other words, paying the farmer and the other extractors of marketable natural raw materials well provides the seed to the value-added processes above. It is that which once super-charged the economy – the real economy. The Mains Street economy. The farmer's money stayed in the community and supported the whole array of local businesses, from the grain elevator and implement company to the butcher, baker, barber, grocer, the local restaurant, and the local banker. The produce that isn't consumed locally moved on to other markets, or up the value added chain toward them, and final consumption there and elsewhere. In effect, these raw materials, since they are new wealth entering into the market channels, represent new money being pumped into the economy from the ground up. It provides the money that circulates in the entire community and supports businesses of every kind, from candle-stick makers to automakers. Distributism, as articulated by G. K. Chesterton and others, calls for capital to be as widely distributed among the maximum number of people possible. And this means farmers and every nature of local owner-operated business, from the barber shops and mechanic shops to small local manufacturing and processing plants. This had always been the key to local prosperity prior, and local prosperity was the key to national prosperity. Every town and community should be a literal beehive of locally own business activity, as they were before our government turned away from policy that supported farmers and individual proprietorships and turned toward economic corporatism and globalism. Wall Street is neither the engine, nor the key, to national prosperity. Gross Domestic Product is not a valid indicator of the economic health of the nation. Neither are evidence of broad-based prosperity. They are false indicators. They are only indicative of movement at the top – government and big business activities which spin in a loop that largely excludes the vast majority of the people. The "business activity" reflected on Wall Street is much more about shuffling wealth back and forth between financial institutions, large corporations, investors, and speculators, than the health of productive industries whose stocks are traded there. Lacking overall real substance, value is increasingly invested in bubble activities, with all the skids are being liberally lubricated with money by the fine people at the Federal Reserve. GDP is a measure of national economic activity that includes activities that have been exported for foreign shores. It's much more about buying, borrowing, trading, and consumption than than real domestic wealth production. Both Wall Street and GDP reflect bubble financial activities as well as smoke and mirror economic activities as positive leading economic indicators. False beliefs that those things are the real McCoy has contributed mightily to the monumental scale and insolvability of our present economic problems. And all of this (government, Wall Street, and the kings of financial capital) is supposedly the great font and source of trickle down! Heaven help us! Look at the derivatives mess; the credit default swaps mess; the mortgage backed securities mess; and all of the other toxic securities that have somehow managed, against all laws of nature, to exceed the global GDP! Under distributionist and trickle-up doctrines, which, after all, are nothing more than common sense applied to basic economics – local economics should, first and foremost, be local. Take the big sub-prime mortgage mess and all the financial toxins that have flowed so profusely from it, for example. This simple common sense rule would have avoided the entire debacle:

That's simple enough. Mortgages should not be considered something that can be bundled and sold to third parties in hopes of a quick buck. The very idea should have been considered ludicrous – and most especially since insane lending practices had already rendered them toxic! Naturally, in a modern industrialized society, there is plenty of room for big business – including giant businesses. But rather than having the Big Three automakers, there should have been the Big Ten or Big Twenty automakers, all of more modest size than the Big Three. Nothing should be too big to fail. Nor should a failure of one auto company, insurance company, or bank, ever severely impact the entire national economy. Distributism is not only about preventing that, it's about making sure that the maximum number of citizens are engaged in the capitalist system in a proprietary role. As one distributionist put it (perhaps G. K. Chesterton), distributism does not say that there is too much capitalism, but that there is too little of it! We need more Mom & Pops and fewer AIGs. JQP August 11, 2010 SPEAKING OF UNITED STATES NOTES... Where did they go? The final disposition... No more U.S. Notes were circulated after January 21, 1971. The Greenback had circulated as currency longer than any other currency note – from 1861 to 1971 – 110 years!* (The first issue of the Greenback, in 1861, before the "legal tender" laws, was in the form of "demand notes") The last notes were printed in 1968. Most were in $100.00 bills, so they would not see much circulation, if circulated at all. The Giegle Community Development and Regulatory Improvement Act of 1994, removed the Treasury's requirement to keep some $322 million in United States Notes in circulation.

In 1996 The Treasury announced that its stock of $100.00 United States Notes, most of which had never really been circulated, had been destroyed. The last technical monetary threat to the Federal Reserve Note was finally eliminated, though the few U.S. Notes still in circulation remain "Legal Tender." See U.S. Bureau of Engraving and printing History of Money: http://www.moneyfactory.gov/historicalcurrency.html Of course, what Congress has once created and then destroyed can be created again. JQP *During the Civil War, the federal government first issued United States Demand Notes (the first greenback notes) which were not redeemable in gold but could be used to pay "all dues" to the Federal Government. When the legal tender laws were passed in 1862, United States Notes inherited the "greenback" nickname. THE BIG PROBLEM WITH FIAT CURRENCIES Naturally, in a culture with a long tradition of monetized gold and silver coin, paper looks appallingly cheap. When literally everybody thought of money as being either gold or silver coin, paper that was not an actual "gold backed note" has always been a pretty hard sell for obvious reasons. Naturally, all of the vested financial interests, i.e., both domestic and foreign banking interests and major industrialists, had traditionally been committed to hard money and a gold monetary and credit standard. In many cases, banks could loan paper, and collect in gold, and always the interest! But there are obvious problems with a strict gold standard too – especially during the quickly expanding economic activities of the modern industrial era. And even more problems emerged with the attempt, in the United States, to have a bi-metal, gold and silver, standard. This, of course, was due to the impossibility of maintaining a fixed value relationship to two completely different precious metal commodities. Finally, paper has won the day. First as gold and silver backed currencies, and finally as our current debt backed fiat currency. And if there was a problem with fiat currencies backed only by the full faith and credit of the United States, look at the problem we currently have with a debt based fiat currency backed by the full faith and credit of the United States! Somewhere there was a workable and sustainable happy medium, but we missed it somewhere along the line and ended up with a banker engineered and operated national and global Ponzi scheme – a disaster waiting to happen. Our present situation is at a point where it seems all remedies constitute "damned it you do and damned if you don't" options. All the big vested financial interests are so committed to banker controlled "debt is money" credit regime that a return to something a little more rational seems impossible. A return to the gold standard seems impossible, while the status quo is obviously impossible to sustain. Wall Street and all of the financial markets spawned there, of course, thrive on the present system. But it has become clear that the system is not only corrupt and unsustainable, but on the brink of total collapse. Rather than representing true commercial and economic values as it should, Wall Street and the stock market have come to represent a caldron of out of control speculative bubble activities. Over-heated air and debt are the basis of most value. It downgrades and discounts real value in favor of speculative bubble and squeak values. To begin a much needed correction, it seems the top priority would be to extract ourselves from the banker controlled debt as money trap. If money can't be something with an intrinsic positive value, at least it shouldn't be something as is an absolute but growing negative value. However we define money (gold, silver, wampum, paper tickets), debt is NOT money – and money cannot be rationally defined as debt. A value neutral money would be far superior to debt money! Obviously, a value-neutral currency can have value by fiat, and function perfectly well in the marketplace. Anybody can visualize the theater ticket analogy. An apparently worthless paper ticket will get you admittance to the theater. The ticket is good for admittance because, by fiat, the theater owner says it is. A Treasury-controlled, purely fiat money such as the Greenback, would at least provide a purely value-neutral currency that doesn't cost us an arm and a leg to put to use. The Treasury is a publicly owned department of our constitutional government. (Whereas it's quite a stretch to imagine there's anything constitutional about the Federal Reserve System.) Of course, we should make sure that the Secretary and other Treasury officials are selected from men dedicated to public service rather that the representatives of Wall Street bankers that we presently have at the Treasury. Nobody can claim that fiat currency doesn't work. We've been using a purely fiat currency since 1971 – for half a century. And before 1971 the the gold standard was largely fiction – a fractional delusion. But, as mentioned above, our fiat money has been of a particularly vicious variety. It's a double-edged sword, since it circulates as debt and demands interest by virtue of its very nature. Even the Federal Reserve debt money system would have worked much longer than it has if Congress and the last several presidential administrations not lost all moral compass, and repudiated every last vestige of fiscal responsibility. While inflation was literally (intentionally and unavoidably) written into our debt money system, most of the inflation we have experienced during the last half century has been the direct result of Congressional spending beyond the means of the tax base, rather than the inherent design flaws in the monetary system itself. In other words, Congress has more blood on its hands than the Federal Reserve bankers. When you come right down to it (and to give credit where credit is due), the Federal Reserve chairmen and governors have managed their jobs remarkably well (at least until 2008 when everything was thrown into chaos). It was Congress that engaged in all the deficit spending which contributed so much to the inevitable train wreck. And it was Congress that voted for trillion dollar bailouts to save a whole class of financial crooks. This, of course, is doubly troubling since it would be Congress that would have to manage any kind of re-nationalized monetary policy. After its performance over the last hundred years we're naturally hesitate to charge Congress once again with its constitutional obligation "To coin [or print] Money, [and] regulate the Value thereof..." The problem with fiat currencies is not embodied in the nature of the currencies themselves, but the issuing authorities. (In our case, that would be Treasury Department, under the supervision of Congress.) Another problem has been the almost universal apparently lack of understanding of the nature of money and credit on the part of Congress. Irregardless, paper is just paper, and a Treasury stamp on it can be meaningful and convey nominal value, or it can be, and often has been in many cases, just a bad joke. Bad government, or even a government with good intentions but bad policies, can destroy anything. Government can literally take a fine purse and make an old sow's ear out of it. Just look what ours has done! Cast pearls before swine and what do you get? Not to call our Congress swine, but they have certainly managed to make a mess out of the most promising nation in the history of civilization. We've had, and continue to have, many fine legislators, but the majority votes have nonetheless consistently delivered up sow's ears. There's no wonder that people like Congressman Ron Paul, Lew Rockwell, Gary North, and the Mises Institute, etc., go into all of the details as to why we cannot trust Congress to do anything right. They consider all fiat currencies patently bad, dangerous, and ultimately destructive – and all of their carefully considered arguments are certainly valid. They make the argument that only gold and silver coin should constitute money, and they make a pretty good case of that too. There is no doubt that gold and silver coin are far superior to any fiat currency, in the obvious fact that they have intrinsic value, just as gold and silver bullion has intrinsic value. But in the end, gold and silver are both relatively rare elements, and gold is particularly so. Rare things perhaps cannot be as common as money must be. So it may makes sense that money should consist of something that is more readily available than gold. As Aristotle once pointed out, money – currency – should not be confused with commodities. Commodities can be used as money, of course, but they are not money unless they are coined, stamped, and proclaimed money by fiat of sovereign, State, or by some other hopefully trusted entity. Pridger readily agrees that gold and silver coin are the only more or less readily available kind of money that can be really trusted. They are both universally acceptable and steadfastly valuable in their own right. Unlike fiat paper or token coin, gold and silver coin are inherently honest money in and of themselves. They are their own value. Therefore they will undoubtedly continue to serve as money long after all our present governments are footnotes in dusty history books. Yet, at least where national currencies are concerned, gold and silver coin have always been fiat too. That is, it was the stamp of the sovereign that made them the coin of the realm. Foreign coin, though of gold or silver, by the same sort of fiat (law), may be excluded from circulation as currency. Coins thus denied "legal tender" status, of course, may still trade on their numismatic or commodity value, but they lack legal tender status within the jurisdiction. During modern times, where several types of currencies have circulated within the same monetary system, actual gold or silver content in coins have always been slightly less than the market value of the coins in terms of their face value. When the commodity value exceeds the face value, people start melting down coins and selling them for their bullion value. When silver prices began to exceed the face value of our dimes, quarters, and half-dollar coins, in terms of nominally gold-backed paper dollars (which were then already fiat dollars as far as Americans were concerned), silver had to be removed from our coinage. This, of course, constitutes the ultimate and latest debasement of a currency. Fiat money can constitute honest money even though it is not a valuable commodity in and of itself, but it depends on both honest and competent government, capable of devising and sustaining a sane and scientific monetary policy. Unfortunately, with an apparent great dearth of honesty and competence, and a great lack of sane and scientific monetary know-how in the right places, gold and silver would seem our only rational alternative. But there have always been problems with gold monetary standards, at least in the industrialized era. Just as the case with fiat currencies, they mainly boil down to the same problems – the same lack of good, honest, and competent administration that has plagued fiat currencies. Trust, and competence are the keys to an honest money system regardless of what a currency is made of. Libertarian gold advocates envision taking the monetary franchise away from government entirely, abolishing all "legal tender" laws, and let the free market handle money creation. But they have a lot more trust in free market forces than Pridger does. Pridger has a lot of libertarian blood coursing through his own veins, but he finds that which passes as the "free market" today is about as badly debased as the currency itself. Indeed, what passes as a free market is a child of the present banker-oriented monetary system, and the corporations that have grown up around it. Markets are often (neigh, usually!) co-opted by the biggest, best, and slickest operators who tend to become the dominate owners. They are no longer really free markets once that happens, and it always does. Pridger can't imagine a nation, or a world, where all money was coined by private individuals and businesses, with all the diverse private coin issues competing with one another for dominance in the open marketplace! There would be mass confusion and monumental accounting problems! And wouldn't the best and shrewdest "gold coin" merchants tend to beat out the competition and become the next generation of gold bankers? That's how the present system – including fractional reserve banking – got started in the first place!

It would all happen again! And the present generation of international bankers, central bankers, and financial plutocrats, that already possess most of the available monetary gold, would naturally have the upper hand! Most "gold bugs" do not care to mention these realities. A gold standard naturally favors those who hold the gold, and the current inflation of fiat currencies works in their favor. Almost all gold advocates are already heavily invested in gold, and are very eager to see gold prices go up. And, naturally, though self-serving, that is a very rational motive for promoting a return to a gold standard. In such case, gold prices would have to sky-rocket in terms of currency of the previous paper standard. Pridger, too, recommends purchasing gold and silver coins and bullion as a hedge against inevitable continued inflation – preferably ten years ago. Ten years ago may have been better, but the present is a good time too. Gold prices will almost certainly continue to rise. And, whatever happens, gold and silver coin and bullion will never disintegrate into paper dust! On the other hand, there is never any guarantee that gold and silver prices will not be manipulated downward again, at least in the short term. With Voodoo economists directing things on the world's financial stage, any number of surprises are possible. Of course, many libertarians are also effective anarchists (not the weird, destructive kind that show up at demonstrations, of course). They claim we would be better off without any formal government at all – that the free market of goods, services, and ideas, can handle everything. That may be true in a perfect world without criminal elements or shrewd business operators to mess things up. But we don't have a perfect world populated with benign people of more or less uniform good will. There's always somebody who will stand up with a big stick, gain a following, and make himself chief. Before you know it, he, or somebody else like him with a bigger stick, is king! We've already been through all of that! That's how the whole "government thing" got started in the first place. Serious government reform is certainly in order, but government itself will not go away. There is a lot to be said for a stable and "uniform" currency under the supervision of competent national government authority, whether that standard is strictly fiat, gold, silver, or some combination thereof. We had a somewhat uniform and stable currency for a period of over a century. It looked uniform and was relatively stable – the almighty Yankee Dollar 1862-1971. But the dollar has suffered a serious decline. (R.I.P. Greenbacks, national bank notes, gold certificates, silver certificates, and even Federal Reserve Notes). The gold standard was even intermittently squeezed in there for a while, along with silver and bi-metalism, but it couldn't last. While American gold coins were minted and circulated for over a century, the official Gold standard, was only in force from 1900 to 1933. That's not a very long track record. Then, after a major correction, it limped along (a fiction to American citizens) until 1971. Without going back to fairly ancient history, Pridger doesn't know of a really successful and lasting gold standard in modern history. Its always been on again, off again – and finally has been abandoned entirely. Silver has done much better as a money standard. The Spanish dollar, the famous Piece of Eight, was in minted and circulation from 1497 well into the 19th century – almost 500 years of continuous use. This was the result of the Spanish conquest of most of what became known as Latin America. Silver was plentiful in their American colonies, and because of the global spread of the Spanish Empire, the Spanish silver dollar became the very first truly global trade dollar. The Spanish dollar circulated freely in the British North American colonies, and was officially adopted as the first "American dollar" after our independence from England was attained – and the Spanish dollar continued to circulation as a legal tender alongside American minted silver dollars from 1792 to 1857. Even the American silver dollar lasted about 150 years (1792 - 1935) and smaller coinage survived until the early 1960s, making the "silver standard" in the United States a 168 year phenomena. With a gold currency standard in particular, there is always the supply problem. Gold supplies simply cannot be depended on to keep pace with combined population growth and expansion of economic activity. Over the centuries gold supplies have fluctuated wildly in terms of other tradable commodities and probably always will. Of course, as gold becomes relatively scarce, a natural deflationary situation occurs and prices in terms of gold rise, and it take less gold to purchase other commodities and products. It may be true that an ounce of gold will buy about the same set of clothes today that it would have purchased in the days of the Roman Empire. But this overlooks one important fact. If all the monetary gold in existence in the world's central bank vaults were turned into coin and circulated as money among the entire global population, gold supplies (and coinage) would be stretched mighty thin. It is conceivable that only the rich would ever find themselves in possession of a full ounce of gold at at one time. Most people would have to remain on a zinc, copper-nickel, or paper standard. The amazing thing is that you can take paper money to the store and buy anything at all with it. This is ample evidence that paper money works. If fiat paper money was removed all of a sudden, there wouldn't be nearly enough gold to place a $20 gold piece in everybody's pocket. Something else would have to be substituted. Paper, perhaps? Obviously, the problems with the gold standard during the modern era became untenable in the face of quickly expanding national and global economies, not to mention the steep rise in government size and spending propensities. These things demanded more money than there was gold and silver available. It couldn't be mined (much less, purchased), fast enough to keep up with demand. This problem, of course, was magnified not only by "normal inflation" but by the very abnormal inflation caused by gross fiscal irresponsibility on the part of governments – of ever-expanding governments showering the people with an ever-increasing array of government bureaus, departments, welfare benefits, various "services," and other entitlements, not to mention the ever-recurrent parade of wars. There are two immutable facts about a strict gold standard. (1) Lacking an 1848 California type gold discovery, it's a very difficult and slow process to inflate gold supplies. And (2), if we had had a real and strict gold standard during the twentieth century, what passed as progress during that century would undoubtedly have been severely retarded. That, of course, would probably have been a good thing. Not only would industrial progress have been retarded, but the wars would have likewise been retarded, or perhaps avoided entirely due to lack of funds. But we must nonetheless face the problems that have resulted from the "American Century" under the gold and the fiat money standards we've had. Those problems are here with us now, glaring right into our face with a penetrating and frightful gaze.

INFLATION Fiat currencies like the Greenback have always been referred to, usually disparagingly, as "inflation money." Inflation, as the term has been historically used, has both good and bad characteristics. It can mean two different things with two different causes and differing effects. And both types of inflation usually happen concurrently, as has been the case in the United States and the world over the last hundred years.

When there is a great lack of circulating money, yet an abundance of people wanting to produce goods and services, progress is retarded or held back. The money supply needs to be expanded in order to accommodate the potential goods and services being held back for lack of exchange medium. To inflate the money supply under such conditions is to accommodate productive activity and commerce which is champing at the bits to be unleashed. In such a circumstance, inflating the money supply to meet commercial potential is a positive thing and clearly has positive effects. Another way of stating this kind of inflation is expanding the money supply to accommodate already available, or potentially available, goods and services. It doesn't qualify as a debasement of the currency (as in the negative kind of inflation does), but rather constitutes a stimulus to fulfill a need – and pave the way for people to fulfill their creative and economic potential.

Clearly, increasing economic possibilities, advancing technologies, expanding market activity, and increasing populations, require more money to function at optimal levels. These things require inflation of the money supply. Only when the money supply is expanded faster than goods and services become, or potentially become, available, does inflation also mean a loss of purchasing power of the money. Only fiat moneys can be easily expanded to fulfill this positive function. A strict gold standard can stand in the way of desirable development (and it can also stand in the way of undesirable development). Ask yourself this question: What if all the riches were there – the fertile lands, natural resources, the willing and able people eager to produce – and there was no gold or silver at all? Would we have remained in the cave? No, of course not! We'd produce and barter, and eventually we would find a convenient way to make exchanges – something handy that can be used as currency. It might just be pretty shells or feathers, or paper do-dads. But it works! And that's what we did. When gold and silver were handy, we used that. When those commodities weren't handy, we stumbled onto "promissory notes" or "promise to pay" notes. On the other hand, the harmful kind of inflation occurs when the money supply exceeds requirement of exchange of already available goods and services, especially when an economy is already working at or near full potential. "Too much money chasing after existing goods and serves." This is the "classic" kind of inflation with which we are very familiar. It leads to the fabled "wage/price spiral" and the unending expectations of increasing incomes to meet and exceed increasing prices and, of course, tax bracket creep. A money supply that is constrained by the availability of gold or silver cannot be easily inflated, because the money supply is tied to metals that are usually in short supply and difficult and expensive to mine. Thus, if there is a gold and silver shortage, and thus a money shortage, it doesn't matter what the productive potential of people or the economy is, there's no way to easily fire them up and get them producing. This, of course, is the positive rationale for a flexible or discretionary money supply. But there is also a very dangerous negative rationale. THE FEAR OF RUNAWAY HYPER-INFLATION We're all familiar with the great inflations experienced in Weimar Germany after World War One, and more recently in countries like Venezuela. Crippling inflation has been the story of the moneys of a whole class of Third World nations. Most often corruption and incompetence have been the major factor involved. But what the scare stories don't tell us is that in almost all instances of runaway inflation have been caused by outside forces (hostile or otherwise), rather than strictly internal factors. The Weimar Republic suffered from severe international pressures and banking shenanigans tied to war reparations that resulted from the Versailles Treaty. Not so coincidentally, most cases of runaway inflation have occurred under the present post World War Two international monetary arrangement – its institutions, doctrines, and modus operandi. Since this international system was developed (i.e., Bank for International Settlements, International Monetary Fund, World Bank, with an interlocking Central Banks, etc.) Third World and developing nations have targeted for assistance, and have routinely been coercively lured and sucked into un-payable debt, by the IMF and other would-be benefactors. That was the cost of enlightened development, industrialization, trade, and full membership in the international community of nations. Uplift! It usually wasn't uplift at all. As often as not, it was a trap from which it was exceedingly difficult to escape. External debt problems, of course, transcended into domestic economic and monetary problems. Under the international system, and the financial and currency markets that have developed, small Third World nations, and some rather large developing nations as well, were ripe for economic attack by friend or foe. A combination of the IMF, private financial powers, and major multi-national corporations, could descend on small nations and effectively take over, manipulating local currencies to their advantage. Sometimes whole national economies and/or domestic currencies have been sabotaged, and economies and lives ruined, by single plutocratic individuals – through their ability to play the global financial game and speculate in national currencies! Leaders and the peoples of many whole nations have literally lost control of their ability to effectively govern, much less be masters of their own economy and monetary destinies. Usually, leaders (along with the favored business interests within such countries), become willing accomplices in the crimes against their peoples. If they resist international pressures and don't "go along to get along," it's either time for international sanctions, or a hostile financial takeover. If its economy is not vulnerable enough for that, and yet important enough for special attention, it's time for outright regime change, if not preemptive military attack. Such nations are generally called "rogue nations" and their leaders often declared supporters of terrorism and compared to Hitler. The major industrialized nations of the West, led by the United States, who set up the present international financial system, thought they were immune to the effects of the game they played. After the collapse of the Soviet Union, they thought the West had gained a great victory and that the great Western Empire was inviolable. But the "best laid plans of mice and men..." sometimes lead to unintended consequences. Runaway inflation is threatening the Unite States today because of a literal witches brew that consists of bad monetary policy, bad economic policy, and bad foreign policy – all of which could have been avoided, and should have been avoided. Our financial, economic, and market situation today is so hopelessly muddled, however, that we don't clearly know if it's going to be hyper-inflation, deflation, or some strange and convoluted combination of both! That sounds like a contradiction of terms and an impossible situation to be in. And it probably is. But that's how bad things seem to be. Inflation can sometimes be an intermittent minor problem under the best government economic and monetary policies. But runaway inflation, hyper-inflation, or uncontrolled deflation (or even a serious fear of them), cannot logically occur under a good and competent government administration. If it happens to us here, the point has been made. WAR AND NATIONAL EMERGENCIES Unfortunately, while an "honest" fiat currency might be the most wonderful invention to come from the minds of men, there is a very serious downside that must be touched upon. Throughout history, fiat paper currencies have almost always been initiated under emergency conditions – times when money was needed badly but gold and silver supplies were short. Sometimes the results are good, and sometimes not so good. The major occasions in American history were:

So all of this points to another of the dangers of fiat currencies. They are WAR currencies! And that's a bad deal when the wrong crew is in charge. In times of major wars, only fiat paper can be stretched long enough or spread thickly enough. Gold and silver could never be stretched as far as Federal Reserve Money has been stretched. Not in several hundred years! There is, perhaps, such a thing as a just, and necessary, war. But there has never been such a thing as a good war. All wars entail wholesale carnage and material destruction. There is never any economic gain, though the victory may gather in the spoils. There is only great economic and human displacement and suffering and the extinguishing of value on a massive scale, though there might be a great surge in productive activity and even innovation. Sometimes positive and innovative products come of war – if we would only use them in rational, peaceful, and constructive, ways! Fiat money could save today's sick and overblown economy, by paying debts rather than expanding them. It could pay workers rather than rob them. But honest and rational monetary policy, combined with wise economic policy, and a humane foreign policy, would be absolutely essential. We cannot correct our economic and monetary mistakes while we carry on unnecessary foreign wars. To attempt to do so would have to allow for continuation of the wars in which we are engaged, and treat them as part of the normal economic activities of the nation. That has never been possible in the past, and it's highly unlikely to ever be a standard of the future. A State in perpetual war will be short lived. We need to return to a national economic and monetary system which will reflect our natural and human resource capabilities, and serve to make the American people productive again – that is, at least productive enough to earn our own way in the world again! We're not doing that anymore now. Have you ever stopped to think of it this way? We, as a nation – supposedly still the richest nation in the world, and certainly the most consumptive and wasteful – are no longer capable of earning our own way in the world! And if we can't do that, we will never be able to get a monetary policy right, because no nation, and no one, can quit working, live on credit, and still expect to get their ducks in order. That's what budget and trade deficits are all about. That's what they tell us (wake up!). They tell us (1) that We the People are unable to support the government that has grown up around us, and (2), We the People no longer manufacture nearly enough of the consumer goods that we consume. Of course, it's not that we can't earn or own way in the world anymore. We certainly could, and we would be a whole lot better off for it. But we simply don't do that anymore. The scary thing is that we may have already forgotten how to be an overall productive society. The last of the most productive generation is now in retirement, or unemployed. As a society, we've forgotten how to work. The social and economic culture has been intentionally changed by fifty years of increasing free trade and globalism. The work ethic is almost a thing of the past. Work? That's what we have immigrants for! That's why we need more immigrants, whether legal or illegal. Most of the good jobs – the easier than backbreaking field work – the millions of factory jobs that once made America great, are gone to Mexico, China, and elsewhere. Most will never return. The American working middle class – the one that made the whole nation prosperous – is effectively gone. The middle class is something entirely different now. It's still pretty large, but it doesn't produce much. It services and consumes. That's become its job. It's greatest patriotic duty is to buy and consume – or maybe sign up for one of the wars. When the Reagan administration started deregulation, "to get government off the peoples' back," he didn't really mean getting the government "off of the peoples' back," or even off domestic industry and business's backs. He was talking about international finance and multi-national corporations – and any domestic producer willing to go international and ship their production offshore. (In fairness to president Reagan, Pridger doesn't think he ever looked at it that way.) Thank Heaven that our farmlands could not be exported, or they certainly would have been! President Reagan admitted that ours was going to become a service economy, and announced that we were entering the post-industrial period of our great history – a period, which within less than twenty years, in which we would find ourselves unable support our own generous nation. He made it sound like an exceptionally good deal. Since then, young Americans have been increasingly educated for the knowledge work jobs that don't exist. Obama is out there promoting that idea right now, thinking education can somehow save the economy and produce jobs. The financial sector enjoyed quite a boom period for a while, providing many extraordinarily good jobs. A whole new wealthy class arose from the frenzied mess (proving that Reagan was right and the globalism is good!). But the boom went bust for a lot of those jobs circa 2008. The best and brightest in our government, and at the FED, however, are blowing bubbles as hard as they can to get some of them back. We may get the foreign version of what we used to produce cheap – but we still don't have the money to pay for them. Fortunately the full cost doesn't show up at the WalMart checkout counter. Nor does the money show up that is borrowed so that we can get that merchandise delivered so cheaply. You see, those imports aren't cheap at all. The true costs are merely hidden in a web of economic policy deceptions. It's impossible to institute anything like a sane monetary policy to accommodate a web of economic policy deceptions. IF ONLY... If we could just recapture our founding principles of limited constitutional government, non-interventionism, and a productive and reasonably protected domestic marketplace, we could once again have a pure gold standard or silver monetary standard. But that's not likely to happen. Since limited government seems to be a thing of the past, maybe it would still be possible to at least have good government. But that's not very likely any more either. But if we could have good and responsible government, fiat Greenbacks could serve as a good domestic currency serving the public rather than costing it. It wouldn't do as an international currency, of course, but could do very well as a "national currency." We'd have to develop a "national economy" again – that is, a productive one – and forget the idea of ruling or policing the world. Federal taxes would be very low, and such taxes as we would have would be aimed at more at managing the money supply and limiting government while funding it. The government, under a Utopian system, could fund itself, of course, but that would be to put far too much trust in our men in Washington. Government should still be kept within strict constitutional limits – meaning that it could not simply fund itself by printing the necessary money. Allowing that would be madness! The currency must be seen and treated as the peoples' money rather than the government's money. That's a very important distinction. The system would be a trickle up system rather than strictly a trickle down system. Money would be spent and loaned into circulation mostly at the grass roots level, at the sources of production. And the government would be supported through taxation in order to keep it strictly answerable to the people, and the ways and means of circulating currency carefully limited and controlled. Means by which the Treasury could spend money into circulation could include...

And much more, including making zero interest loans to state and local governments. But there should be strict limits. With major federal payrolls and "entitlements" removed from the tax ledger, taxation to fund the core government would be considerably lower than today. Today borrowed obligations supposedly to be paid in future taxes, fund almost everything – an impossible situation that must be remedies soon or we'll ultimately effectively be sold into slavery to our creditors. SOCIAL CREDIT Some authors and monetary thinkers like Ellen H. Brown (Web of Debt), and Steven Zarlenga (The Lost Science of Money), who favor a Greenback-like system make favorable mention a form of "Social Credit" or "National Dividend" that would be possible with a Greenback-like national currency. Without getting into how it would work and why, a national dividend would be sort of a return on the economic activity of the nation – the national profit, if you will, as in a business – which could be paid as an annual dividend (or even a monthly stipend for that matter), to all citizens. This idea isn't new, and Pridger has read of it long ago in books he cannot specifically name at the moment. It may even be a nineteenth century idea, or even earlier. From Pridger's standpoint, the national dividend idea is a slippery slope and would be counter-productive. In theory, under a purely fiat system, everybody could be paid a full salary whether the "national economy" turned a profit or not – just as the government could fund itself by printing money. The danger that Pridger sees, of course, is that paying people for nothing might encourage them to do nothing. The work ethic is already in taters. But if we are ever to become a productive nation again, at some point were going to need a lot of eager workers – and we don't want to have to continue to depend on new immigrants! JQP August 4, 2010 GOOD "MONEY AS DEBT" VIDEO

IS THE GREENBACK IS STILL AN ANSWER? When it comes to saving the American economy, we still have the expedient that old Honest Abe Lincoln resorted to during the Civil War. That, of course, is the good old Greenback – Treasury Notes issued to serve as currency. They were called "United States Notes." They circulated from the Civil War until the late 1960s or early 1970s, and still officially constitute part of the monetary supply, though they no longer printed and are seldom seen today. After the Civil War, United States Notes were called in but survived as a small increment of our money supply for another century. Greenbacks were given a new lease on life with the Resumption Act of 1875 (which resumed convertibility of dollars to gold for the first time since 1861.) It became effective in 1879. And, due to public pressure, it included renewed issue of Greenbacks.

Federal Reserve Notes (as our other forms of paper currency), were made to look like Greenbacks and both are printed by the Treasury, but they are very different except in their appearance and use as currency. Don't confuse Greenbacks with the bank "national bank currency" created by the National Bank Acts of the 1860s). The National Bank Acts and National Banking System were actually a "banker" takeover of money issue even as the Greenback "legal tender" laws apparently sought to free the government and nation from the grasps of bankers. The National Banking System survived until 1935, dying during the Great Depression when many National Banks failed. Let it suffice to say that the National Banking Acts were contemporary with the Greenback "Legal Tender" laws but were laws that favored private bankers aimed at countering and limiting the Greenback initiative, and National Bank Notes were, of course, Treasury printed "Bank Notes" issued by specially chartered "national banks." They constituted a significant precursor the later "central bank" Federal Reserve Notes. The difference in the Greenback and Federal Reserve Note is simply stated. The Greenback is simply government issued money – the peoples' money – and Federal Reserve Notes are banker indebtedness notes – pure debt credit money. The first is simply a "ticket to the show" and the other is a "ticket to the show that you still have to pay back, after the show, with interest."

Never forget that while we still refer to all of