|

|

PRIDGER |

|

E-Mail |

John Q. Pridger's

|

|

BUY AMERICAN:

http://www.usstuff.com | http://www.madeinusa.org/

| http://www.stillmadeinusa.com/

| http://www.buyamerican.com/ |

|

|

|

PRIDGER |

|

E-Mail |

John Q. Pridger's

|

|

BUY AMERICAN:

http://www.usstuff.com | http://www.madeinusa.org/

| http://www.stillmadeinusa.com/

| http://www.buyamerican.com/ |

|

|

Pridger's Web Host Important Links BLOG DEC.

2008 JUL-DEC.

2007 DEC.

2006 |

Saturday, 31 January, 2009 A CROSSROAD IN OUR NATION'S HISTORY Not since the rise of Adolf Hitler in Germany has a national leader come to power as the result of such irrational public adoration as President Obama received.

Has not this plunder and waste already occurred? Were not the Huns and Vandals engendered within our own country by our own financial institutions, stock market, mortgage, and derivatives wizards? Did it not occur over the span of the twentieth century and to the present? Were not the Lincoln and Franklin D. Roosevelt administrations temporary seizures of power with a strong hand during the ninetieth and twentieth centuries, though they were not destined to succeed? Had not Thomas Jefferson also warned us:

Is President Obama going to become our third, and perhaps last, dictator? Will he become our Caesar or Napoleon? Does he not seem to have the popular mandate?

All humor and satire aside with regard to personal oaths to the Furhrer, it is nonetheless likely that at some point Barack Obama will be required to resort to emergency dictatorial "War Powers" similar to those used by Franklin D. Roosevelt soon after he took office in 1933. The unprecedented nature of the present national and global economic tsunami will practically mandate such a move. The big irony is that the man who has come to power at this crucial time in our history is without a doubt the least experienced, least accomplished, and most unknown personage ever to have been elected to the office of the president in the history of the nation. He was elected on personal appeal alone. Perhaps we should say he was elected on faith. Our problems today are many times worse than the ones Roosevelt faced, and they are not going to be solved by ordinary means. Unlike the nation of FDR in 1933, our nation is now both bankrupt and, to a great extent, de-industrialized. It's in a position of extreme vulnerability for several reasons. It is not only incapable of earning its own income, but incapable of self-reliance. The proclaimed "American way of life" has become one of conspicuous consumption and waste, purchased on credit. Yet the nation is engaged in two costly distant foreign wars, with troops and bases in about 130 other nations. The public – with patriotic consumption on the wane – is demoralized and no longer a cohesive and unified body politic – culturally, religiously, or politically. None of this was true in FDR's day. Our nation is so demoralized that a Hitler might easily have come to power had we had one. But the election results are nonetheless testament enough to our national malaise. We no longer have rational leadership anywhere in government. As has become usual, the only candidates with any foresight and knowledge of what has been going on in this country were culled out of the running early. Barack Obama, the most unlikely candidate of all was chosen, whooped up, and elected – his agenda, "Hope!" and unspecified "Change." Franklin D. Roosevelt once said, "Nothing in politics happens by accident. If it happens, you can bet it was planned." Undoubtedly, Obama has come to power for a purpose. No doubt that Obama will be able to honor his promise of change. "Change is coming!" But we don't know what kind of change is coming. Since our nation has been under the effective control of financial capitalists for 95 years, it isn't too much of a stretch to equate economics with politics, and perhaps conclude that, "If an economic meltdown happens, you can bet it was planned." But if this is so, what is the purpose? Could it be so a president could gain the dictatorial powers necessary to usher in the next stage of "the long held aspirations of mankind – a New World Order"? John Q. Pridger

LOOSE TALK ABOUT "AN ECONOMIC PEARL HARBOR" One wonders who the enemy would be?

The Crisis of Common Sense: Is It So Difficult To Understand

The Financial Crisis?

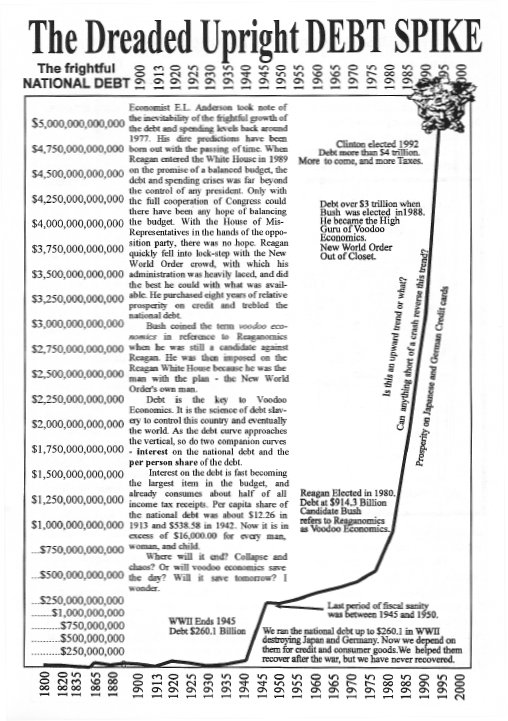

Global Financial Domination: The $8.5 Trillion Chip Friday, 30 January, 2009 THE REAL ECONOMY VS. FINANCIAL CAPITALISM When Congress passed the first $700 Billion financial rescue package a few months, it's stated purpose was to rescue the financial capitalists – essentially big bankers, and Wall Street interests. But we heard objections decrying the bailout for lack of aid for the "real" economy. Since then we've heard more references to the "real economy" – as if we have two economies, one of which isn't "real." The economic stimulus package President Obama is eager for is supposedly intended to come to the rescue of the "real" economy – or at least alleged segments thereof. In fact we do have two distinct economies. We have the work-a-day economy and the financial economy. The work-a-day, "real economy" earns its own way. The financial economy masquerades essential to the real economy, but really it is 90 parasite. During the last hundred years and more, the two have been increasingly blurred into one economic whole, since the real economy has become dependent on the financial economy in order to function. But it is unnatural for a viable complex organism to be dependent on parasites that draw on its blood for nourishment. The host may thrive with a few parasites – they might even be useful – but when the parasite becomes stronger than the host, the host is doomed. The real economy is a natural occurring phenomena combining both grass roots and corporate economic activity. This includes farm and factory production (small and large), forestry and fisheries, value added activities, wholesale and retail trades, transportation, and building trades. The individual truck gardener who sells his vegetables at a roadside stand are a part of the real economy, as are truck drivers, and mom and pop merchants and service providers. And so are the corporate big boys such as Walmart and the Big Three automobile manufactures. Additionally, other activities can be defined as part of the "real" economy as well, though they are not necessarily productive in nature and don't actually earn national income. These includes a whole array of service industries as well as the more or less arguably essential public sector activities, from kindergarten teachers through the array of civil services, to the President of the Republic. Government, to an unavoidable degree, must qualify as part of the "real" economy simply because social chaos would probably result if we didn't have it. The financial economy operates on a different plane, with different mechanics and purposes. It has two main purposes. First, it is essentially a parasitical economic machine that exists only for gain and power which must be derived from the productive labor of the host (the real economy). It's second, but no less important, purpose, is to make the host beholden to it, and dependent upon it. It must make itself essential lest it be brushed aside as quickly as we would divest ourselves of ticks and leeches. Modern financial capital's genesis was in the Middle Ages when, using its previously gained power over the purse, it established large banking houses. In time it invoked fractional reserve banking, and the wonders of compound interest – and finally its establishment of itself as the "money power" in the modern world. In short, it first made itself useful, then addictive, and finally totally indispensable. The financial powers centered around the rulers and ruling classes, underwriting personal and "public" loans to rulers and nobles who were always in need of more money than they were able to tax, to enforce their rule and conduct their various wars of conquest or defense. There is, of course, a long and interesting history here, which included the era of great exploration, colonialism, and the advent of the limited liability company to carry out these often very profitable adventures. We won't get into much of that history here. Throughout the history and growth of financial capital, the "real" economies (i.e., the productive sector of society), largely functioned without financial capital's influence or help. The ruling class taxed the peasantry, and thus enriched itself, but never enough to do without the financial class. But the peasantry, or the yeoman farmer, and village shop keeper, did very well without financial capital. Goods and services funded their activities and these were what made up the real economy. As the industrial revolution progressed through the 19th century, and the scale of manufacturing activities increased, the services of financial capitalist became very handy, as did the organization of limited liability companies. But ever the large corporations didn't really need the service of financial capital. The idea was that individual investors financed initial business operations through the purchase of shares of stock – the same way new banking ventures were initially funded. Businesses generally either succeeded or failed on their own merits. If they succeeded, and made enough profit to satisfy the stockowners, they could, and did, use excess profits (savings), to fund expansion of the factory or business. This was called capital formation, and it was through capital formation that most of our industries once expanded, and many of them became lasting national icons. The golden rule for all business enterprises was, "Spend profits only, never capital. And expand only on savings." Generally they did not borrow money from bankers unless it was an emergency situation, and then the loan would be paid off as quickly as possible. But when big, often state sponsored, enterprises began to evolve, such as canal building and railroads, the initial investors and owners were increasingly members of the financial class or their proxies. Local banking has always been useful, but in the early years of our republic most private bankers were not connected to the Eastern Banking establishment or international bankers. When a person wanted a small loan to open a store or get a crop in, the local banker usually obliged him, provided he pledged sufficient assets to protect the bank from default on payment. In any case, the loan customer, and his credit worthiness, was usually well known to the banker. Local merchants had always extended a modest amount of credit to their customers, who were also neighbors. But as large mercantile corporations such as Sear and Roebuck began to come on the scene, the practice of extending person credit became part of the sales pitch. "Buy now and pay later," became a national norm for the whole array of goods and household appliances. The idea of extending the realm of financial capital into the lives of ordinary citizens began to jell. Perpetual personal debt of large segments of the population began to pay big dividend streams to large corporations. In time, the big banks started getting in on the action by issuing credit cards, so they could get "their cut" of the action of the personal credit phenomenon. Thus even ordinary individuals began to have personal credit dealings with major financial capitalist bankers. Home mortgages became big business, especially after World War Two, which eventually drew in big financial concerns. Over the term of a 30 year mortgage, a bank could collect several times the purchase price of a family's home, with almost no risk and no effort at all. The only risk was default and foreclosure. The Civil War had spawned an unprecedented proliferation of large manufacturing enterprises wherein financial interests where increasingly involved. And in every case where financial interests were involved the trend was to expand the business on debt financing wherever possible. If any profitable industrial or service enterprise could be kept perpetually in debt, the bankers would have a steady income stream compliments of the workers and stockholders. There became the inevitable marriage between industrial and financial capital, aimed at squeezing more and more profit out of every corner of every market using every angle conceivable. The stock market was set up by financial interests, as a means of trading stocks in private corporations. It soon evolved as the speculative marketplace that it remains today, with a peculiar relationship to the real and financial economies. The futures markets followed, supposedly to have a stabilizing effect on commodity prices, but this market too was invaded by the speculators and its alleged purposes subverted. Aside from the money power itself, by far the worst aspect of financial capitalism, married as it is to industrial capitalism, is the power to allocate capital to industrial and commercial enterprises that promise to be the most profitable to it. Often this became mis-allocation of massive credit resources, allocating massive resourses and economic power to the largest, most exploitive, and predatory enterprises. It enabled over-development of certain corporate systems whose scale often destroyed both the environment and small scale free enterprise too, as capitalism is by nature both predatory and cannibalistic, gobbling up smaller, more vulnerable enterprises. Of course, in the wake of World War Two, the massive military industrial complex came into being, with financial capital playing an ever-increasing role in allocating massive credit resources with official government favor. When the nation and the world abandoned the gold backed monetary standard, financial capital was unleashed as never before possible or imaginable. As of that moment there was literally no longer any real limit to the credit that could be showered down upon favored industries and organizations. The government itself took the lead in unabashed spending. Congress literally forgot what fiscal responsibility meant, even though every dollar it spent resulted in unprecedented and obscene levels of public debt. From that time on, the primary fiscal responsibility of Congress was increase spending and periodically raise the debt ceiling before the debt punctured through it. The whole country seemed to follow Congress's lead. The New World Order was finally unveiled for all to see – the Wonderful New "intricately interdependent" World came on line – financial and industrial globalism with free international trade. It was no longer considered patriotic for Congress to protect either the Constitution nor the nation they were bound by oath to protect. The American marketplace was virtually officially made the dumping ground of the world. As for Americans losing their jobs to foreign competition, they could get retrained to become "knowledge workers." By these processes monstrous businesses like Walmart have been able to displace literally hundreds of thousands of small commercial proprietorships as well as help shift the tide of production from domestic industry, and American workers, to offshore industry and foreign workers – all in the righteous quest of "delivering to the consumer the best products at the lowest possible prices." This has repeated itself throughout the economy over and over in almost ever field for many decades. All of this being the case, real wealth does not originate from within financial capitalist realm. No wealth is created by bankers, financiers, central banks, treasuries, or government, regardless of how many times you repeat "trickle down." Real wealth is created much nearer the common man and originates within a small by well defined sector of the "real" economy. All real wealth originates as raw materials from the earth, the produce of the farms that feed us, delivered up from mines and fields by the hand of labor. This initial tangible wealth is refined, processed, transformed, fabricated, manufactured, built, and transported, by labor. This, and this alone, is the source of all real wealth that has ever been created in the world since the sunny day God plopped Adam down into the Garden of Eden. It is this wealth that supplies the material for all value added commodities, enhanced by real economy individual and corporate enterprises, and that wealth is multiplied as it makes its way up the economic chain, where it then might trickle down again into other less productive sectors of the economy. It has been calculated that for every dollar earned at the farm or mine level, seven dollars are generated, or facilitated, as raw materials and products move up the economic value-added market chain. This multiplier increases with the state of the arts in production. But if you short-change the producers at the source of initial production (as, say, in a cheap food policy), the same multiplier applies, in reverse, depriving the economy of seven dollars of earned income for every dollar the primary producer is shorted. To the degree the economy is fed by foreign imports, domestic "earned income" is disrupted and becomes increasingly illusionary. Wages go to foreign workers, and profits go to corporate owners rather than domestic workers, and the resulting wealth bubble at the top is debt-generated – for which debt the American taxpayer is billed every April 15th. Financial capital naturally tends to increase in inverse proportion to real earned income, earned by under-compensated or unemployed labor. Financial capital is enriched at the expense of under-paid and under-employed domestic labor, as well as underpaid foreign labor – and their greatly increasing level of wealth is, of course, unearned income. In this process, wealth is transferred from producers to to financial capitalists and corporate industrialist who march to their tune. The bottom strata of the real economy suffers proportionately. Thus the de-industrialization of the America economy even as the stock market continued to climb, right along with the national debt, into the stratosphere. But you cannot build real wealth unless it is produced and priced in the domestic marketplace. A huge percentage of our domestic GDP is illusionary. It is neither wealth nor earned income – it's debt, with no redeeming real economy underpinning. Almost half of our GDP is government generated, with government now the largest single employer in the land. The chickens have finally come home to roost and let us know that our financial capital model is not working. I never worked because it was based on fraud and smoke and mirror economics – Voodoo Economics. It's time to divorce the real economy from the financial profiteers and manipulators. It's time to unleash the natural abilities of the real economy, first and foremost by providing it with an honest system of exchange. John Q. Pridger Thursday, 29 January, 2009 STIMULUS PACKAGE BREEZES THROUGH THE HOUSE Last year the outgoing administration ram-rodded a $700 billion emergency bailout package through the Congress – to prop up the bankers and the crooks. This, was in addition to previous bailout moneys spent to bail banks and insurance companies out, and doesn't include the interest that must be paid on those funds. Now there would seem to be some very funny things going on here. Both banking and insurance are the most profitable businesses in the world. Money literally rolls in and out under mathematically derived formulae and rules that insure profits on every thing they do. Of course badly run banks can fail if they have become too greedy and have made too many bad loans – but generally speaking, banks and bankers represent the rich elite of the rich elite. And we are talking about the biggest of the big – the very apex of the banking and financial pyramid! But incredibly, the poor taxpayer, and his children and grandchildren, are being made to underwrite these mega-banks and mega-bankers, and insurance companies – the richest of the rich. Yet we were told that we've got to do it, and "DO IT NOW!" lest the entire sky cave in on us. No time or need to think – the bankers have already figured it out for us. "Just sign on the dotted line, and we'll take care of the details and fill in the blank spaces," they told us. The president and Congress took their word for it and hastened to plunge the citizenry into over a TRILLION dollars of additional debt – on top of the $11 Trillion debt we already had. It doesn't take a rocket scientist to see that there is something direly wrong with this picture. Not just wrong, but downright unjust and criminal. But, we are told, this is the "system" and the system has to be fixed and fixed in a hurry. Now Barack Obama, the hope of the future, is on track to getting his additional $819 billion "economic stimulus" package through Congress. The actual price tag of this alone, plus interest, will probably exceed $1.5 trillion. But this is just the beginning of the "stimulus." They tell us that many more TRILLIONS will be needed to get us out of the financial crisis and save the poor working man – and the non-workers too! When we talk Trillions of dollars, we're talking big money. Our entire national debt didn't reach the $1 Trillion level until 1982. Since then it has increased to $11 Trillion, without considering the additional Trillions recently appropriated. Interest alone on the National debt for the fiscal year 2008 was $451.2 Billion ($451,154,049,950.63, to be more precise). The entire national debt had not reached that amount until 1945. (It was only $43 Billion in 1944 – and jumped to $258.7 Billion in 1945.) The interest on the national debt has doubled since 1988 when it was $214.1 Billion. This doubling of the interest took 19 years. But we expect a federal annual deficit of about $1 trillion in fiscal year 2009, and probably more than that. So, it appears the doubling time of the debt and the interest is decreasing by leaps and bounds. We will be compounding the national debt by Trillions of dollars per year rather than a Trillion in 206 years or 95 years (since the Federal Reserve Act was passed). Can we really do this? Certainly not for very long. The game is up – but we're still trying to play. We have regressed far beyond the platitude and apology for deficits and a growing national debt. We no longer "owe it to ourselves." We never did really owe much of it to ourselves, except insofar as "ourselves" included American banks and financiers, institutional investors, and a few wealthy individuals. We don't pay our income taxes to ourselves, we pay to the IRS mostly to the profit of our financial overlords. Interest on the national debt is already the third largest item in the budget, and it will soon outpace the amount we spend on social welfare programs and defense. In time it will become the biggest single item. Interest on the national debt will soon outpace our entire national tax revenue stream. That's when we will not only be totally bankrupt, but in default. Some sort of foreclosure is certain to follow. Though it's already very late in the game, it isn't to late to fix the problem. It's better to actually fix the problem now than wait for default and foreclosure. In fact, though fixing the problem would be painful, and make a lot of international bankers mad as wet hens, it would be relatively easy. This is the time to do it. Bankers and their central banking systems, and the raft of financial "industry" hangers-on, have never been as exposed and discredited as they are right now. They can't be allowed to dictate the fixes. If we continue to allow that, we're merely in for a bigger fall just a little further down the line. When we are no longer able sell our government treasury securities, the only alternative is to simply print money. That circumstance is bound to come. We're probably already there now, hoping we can "sell the debt" it represents later. But every dollar printed is still a debt dollar. Who owns that debt is immaterial, the public is still bound by it, plus interest. Many foreign holders of our debt are getting very worried that we might merely be "printing money." If we are doing that, they know the dollar is fast becoming worthless as an international reserve currency. But guess what? The American dollar doesn't have to be the world's reserve currency. It was a big mistake in the first place, making it impossible to properly regulate our own domestic currency supply for our own benefit. The American dollar should be an "American" dollar again. Let the international community settle on something else for a reserve currency, such as the traditional gold and silver, or their already long existent Special Drawing Rights (SDR), or so-called "paper gold" trade and international balance of payments money (presently certificates representing a mix of the world's major currencies). It's time to break free of the "cross of massive public debt" and reclaim for our nation its right and sovereign duty to provide the American people with a "national currency" of our own. We already have the proven model in the Lincoln greenback – United States Notes. Those are the kinds of dollars we should be printing now rather than Federal Reserved Notes. And they would circulate as they did in the past, during the Civil War and in limited amounts right up to the late 1960s. They wouldn't ad to the national debt. Greenbacks are "bills of credit" and "social credit" dollars, based on the full faith and credit of the nation. They are non-interest bearing Treasury Notes in denominations used as currency. They are just like other Treasury bonds – that we now use to "secure" debt – but issued as a circulating currency at little cost and no interest to the public. The public would readily accept greenbacks as it did in the past. It was the United States Note, the famous and enduring greenback, that set the standard for our various national currencies. National Banking Notes were designed to look like them, as were gold and silver certificates. As were Federal Reserve Notes. They all looked alike so that we could have a "uniform" national currency. The public accepted Federal Reserve Notes because they looked like greenbacks. In fact, we continue to call them greenbacks for that reason. But only true greenbacks are "our own money." They represent value in the marketplace. Had Franklin D. Roosevelt simply abandoned the gold standard and spent United States Notes rather than gold backed greenbacks and Federal Reserve indebtedness notes, he would have been able to successfully "prime the national pump" and get the economy going again, and the Great Depression would never have been. But he didn't. He allowed himself to be hamstrung by so-called "monetary orthodoxy." His national economic recover efforts were severely hobbled by the dual demons of banker debt money and the bankers' fictitious gold standard. He had the power to overcome those limitations, but chose to pleasure the bankers instead. This was the great irony of the Keynesian deficit spending policies that FDR pursued, and which we are still pursuing. The money used, and the entire banking monetary establishment behind it was fundamentally corrupt. So his efforts were doomed to failure from the beginning. Deficit spending is possible with the greenback, because the money does not have to represent either expensive precious metals or public debt to profit seeking bankers and profit "investors." Under a properly managed fiat greenback system, money is "currency" to used for exchange. It isn't an expensive commodity in its own right. It merely represents exchange value, and under an honestly regulated system its purchasing power can be maintained. Under a greenback system, deficit spending would not really be deficit spending as we think of it today. The value of the money is its exchange value, and the enduring value of the public and private works it facilitates. Greenbacks automatically discharge the debts they are spent to satisfy. It doesn't have to be paid back – it continues to circulate, facilitating both exchange and production. That's the big secret bankers would rather we never learn. John Q. Pridger Wednesday, 28 January, 2009 COMMON SENSE NEED NOT APPLY Unfortunately, common sense in government policy and finance is no longer applicable. Things like increasing spending while reducing taxes with no hope of ever getting the budgetary process under control have become the norm. Spending our way out of economic trouble – long in the making – with borrowed money is the only avenue considered. None of this makes any sense – certainly not common sense. Prosperity through consumption, rather than production, has long been the norm known as the new "American way of live." Prosperity through debt, debt manipulation, and ultimately nothing less than Voodoo Economics. "Toxic" bank assets and investment vehicles have become overwhelmingly prevalent. Pridger recognized derivatives as the HIV/AIDS of the financial system almost two decades ago. He saw the idea of borrowing and spending one's home equity as crazy. He saw the advent of no money down and interest only housing mortgages as a form of insanity. It was obvious that accelerating deficit spending while subsidizing the export of productive industries and jobs as economically suicidal. Back in the 1960s Pridger was perplexed by the fact that Japanese cars, made of American steel that had to be shipped 6,000 miles across the Pacific Ocean, could somehow be shipped the same distance back and still undersell American cars. The same thing was happening with televisions sets and the booming field of "new" electronic devices. Pridger didn't really understand the mechanics nor economics of it then, but he instinctively knew something was wrong. It didn't really make sense. It seems every generation of Americans has its own war to associate with its formative years. Pridger's was the Vietnam War. He first visited Saigon in 1962, as a navy sailor, and later, as a merchant seaman, made it his home port. He worked for a time for RMK-BRJ, the famous "Vietnam Builders" whose direct corporate descendent, KBR, are now supposedly rebuilding Iraq and Afghanistan. Pridger was in Vietnam simply because he had become enamored with the the Far East, and Vietnam happened to be the place where expats could find good jobs, either ashore or afloat. Yet Pridger's question at the time, however, was, "Just what are we, as a nation, doing waging destructive and bloody war here?" The official answers, "propping up the dominoes", and "fighting for freedom and democracy", somehow didn't ring true – especially when it became obvious that we weren't really fighting to win (at least not over communism). That became even more apparent when, in 1972, we began openly subsidizing the Soviet Union with our classic "wheat deals." In 1973 it became obvious to Pridger that our nation was in dire need of a national energy program to avoid becoming dependent on foreign oil producers. OPEC went out of its way to give us timely notice. Our leaders didn't get the message. By 1975 we got some untimely notice that unnecessary foreign wars were not only excessively costly in lives and treasure, but often disastrous quagmires. In that year our great Vietnam project came crashing down around our ears. Our leaders have since forgotten that lesson. Pridger worked in the offshore oil fields of the Far East for a few years in the early 70s. Indonesia's offshore oil fields were already producing large quantities of oil for export and more were being developed at a rapid pace. Pridger found himself asking "What will Indonesia do after it has developed and found that it needed its oil for its own use?" It appeared that it would probably be all gone by then, and I surmised that it would have to import its oil from elsewhere – probably at prohibitive prices. In the mean time we, the Japanese, and Europeans, needed their oil. Something was wrong with that picture. Toward the close of our Vietnam adventure, our balance of trade began to invert from a positive to a negative figure. The richest, most productive, nation in the world was beginning to import more than it exported. And in about 1980 the richest nation in the world went from being the world's greatest creditor nation to the world's largest debtor nation. Whoa! How could that be? The richest, most prosperous, nation in the world? Yet we were giving things away right and left. Foreign aid was supposedly continuing to flow to all points of the globe. It seemed the whole "free world" was on some sort of welfare program, compliments of the U.S.A. Something was obviously going woefully wrong in America. President Reagan proudly announced that we were entering a post-industrial era – that under a "new international economic order" ours would become a service economy. Pridger, who loved Reagan's conservative rhetoric, remembers asking himself, "This is progress?" Somehow, something was not ringing clear. Even supply side, trickle down economics didn't sound right. "Free trade" and "global free markets" sounded pretty good at first ("free" being one of those famous advertising hook words), but intentionally striving for "international economic interdependence" sounded suspiciously like repudiating the idea of national economic independence, and perhaps more than that. This definitely seemed counter to plain old common horse sense to Pridger – and so it proved out. Reagan, who campaigned on a "balance the budget" platform, didn't balance the budget – not even close. He was lucky enough to take credit for ending the double digit inflation of the Carter years. But that didn't stop the real inflation of the currency and thus the national debt. The national debt reached the astounding $1 trillion benchmark during his first term. But business began to boom, because the money changers, in league with the multi-nationals that had grown up around them, were hard at work on a New World business Order. The era of mega mal-distribution of wealth, through massive credit availability, and trickle-down processes, had gone onto steroids. The Reagan (Bush and Clinton) prosperity looked awful good, but it was purchased at a very high price. In 1985 Pridger had a free trade eye opener, when his ship called at Japanese ports to load nice new yellow "Caterpillar" tractors and other CAT heavy machinery for export to the United States – the home of Caterpillar. These were "American Products Produced Abroad" (APPA)! "American products" produced abroad? How could that be? Not only that! We loaded huge rapid transit train coaches for the Atlanta, Georgia, Rapid Transit System! Pridger's thoughts were, "What's wrong with the people back home? How can these things be built in Japan and shipped thousands of miles across the Pacific Ocean, and across the country, when we have all the factories we need to build them (surely much more economically), at home?" It had long before dawned on Pridger that our government was betraying America and American workers through its so-called free trade policies, but this was nonetheless a wakeup call! We weren't just importing compact cars, TVs, and VCRs, but everything large and small, that we were once perfectly capable of producing for ourselves. Obviously, I reasoned, there must be profit in it, but it didn't make sense or even seem credible. Of course, it was profitable for those people engaged in the business – because, while it might be cheaper to purchase bulldozers and train cars from Japan rather than from factories in Illinois, the cost differentials and profit margins of free trade were being unwittingly underwritten by the lost wages American workers and the generosity of future generations of American taxpayers. The environmentalist were happy to be rid of America's "dirty" industries. But those dirty industries, dirtier than ever, and still growing, were merely moved to Mexico, China, and elsewhere, at economic and environmental costs that they didn't even begin to foresee. Initially, they didn't seem to care, for the do-gooders were happy to be giving the rest of the world a leg up. Then enter the specter of global warming in the way of over-development blowback on a global scale. We could have cleaned up our own industries – it was our duty to do so (and certainly before passing them on!) – but the factories in Mexico, China, and India are not subject to the whims and wishes of American do-gooders. So in the end, we have passed most of our worst industrial plagues, financial viruses, and economic infections, on to our friends in Europe and Asia. And in doing this we were also committing industrial, economic, and strategic, national suicide. All of this, of course, hastened the closing moments of the massive financial debacle that has recently manifested itself – the shock of collapse of a long ongoing, sacrosanct, Ponzi scheme – one that might have successfully run another hundred years had Congress not forgotten the meaning fiscal responsibility and some facsimile of loyalty to the American people, not to mention common sense itself. All of these thing were obvious years ago – even to a functionally illiterate maritime hillbilly. What was wrong with our politicians, the Washington brain trust, great university academics, and their multitudes of think tanks? It seems the social Utopians on the left, and the corporate Utopians on the right, have colluded to do us in, in the name of One World togetherness. One for all, and all for one, until the dry sand shifts under the great houses of cards, and the great hot air bubbles begin to develop un-patchable leaks.. Take the simple case of the housing and real estate bubble and the toxic mortgages that were pawned off on both domestic and foreign investors. They are given credit for starting the house of cards coming down. In a rational world, where real common sense rules in both personal and business affairs, a home mortgage is a very simple, free market, arrangement. It's a private affair between the home buyer and his local bank as lender. There's no rational way that such a thing could ever bring the national and international financial world down. But, between the Washington and financial world's brain trust, they figured out how it could be done! Instead of a real economy driven at ground level by a hundred million producer/consumers, millions of small family farms, hundreds of thousands of small mom and pop businesses and individual proprietorships, all producing and looking out for their own personal and community oriented interests in a true nation free market system, our leadership opted for a global economy driven from above by huge transnational corporate mega-systems – industrial, mercantile, service, and financial. Most of these mega-systems have become too large to be allowed to fail – for if they do, there is big trouble and massive dislocations. And that's where we are today, with big trouble and massive dislocations effecting the entire global population. All because of a great lack of common sense at the highest policy making levels. These mega-systems are supposedly the epitome of modern efficiency – delivering the goods that consumers want and need at the lowest possible prices. But guess what? Those systems are not nearly as efficient as they have been made to appear. They haven't been paying their own way – not by a long shot. It's all been a smoke and mirror game buoyed hot air balloons holding up an elaborate Ponzi scheme. Building and having these mega-systems has cost us tens of trillions of dollars that have yet to be paid, and paid with interest. Now our new president is faced with the chore of saving this fundamentally flawed megalithic mish-mash of systems within systems. He has an impossible job, but is doing the only thing open to him – throwing tens of billions of bad money after trillions of bad money at fundamentally flawed systems. President Obama, as with the late Bush administration, is trying to "jump start" the economy, rather than fix it. It isn't fixable. The effort is merely a desperate effort aimed at bringing a modicum of stability to the banks and financial markets first and foremost, and some small degree of relief to the increasing numbers of unemployed. It's an ironic situation for the once greatest, most democratic, richest, most productive, most prosperous, and economically powerful nation in the history of nation states, to be in. Bankers and New World Order people are essentially in charge, of course, and they won't settle for anything less than jump-starting their own global Ponzi scheme first and foremost. John Q. Pridger Tuesday, 27 January, 2009 OUR MONEY SYSTEM IS OUR PRIMARY PROBLEM Our president has just appointed Tim Geithner, the former head of the Federal Reserve Bank of New York, to be his Secretary of the Treasury. This long ongoing incestuous relationship between the Treasury (a constitutional branch of government), and the Federal Reserve System (a "federalized" private banking cartel), pretty much insures we will remain nailed to the cross of perpetual compounding debt. Federal Reserve bankers in the Treasury, of course, are naturally likely to be more focused on bailing out fellow bankers and financial interests than getting America back onto a sane monetary and fiscal standing. There will be no serious look at real financial reform, and all efforts at correcting our economic malaise will focus first and foremost on bailing out, propping up, and rescuing the bankers rather than delivering justice to the people. In this most important area, our new "change" president has surrounded himself with more of the "Same."

The statement "The New York Fed presidency is on of the most powerful positions in government," says an awful lot. How is it that a banker (any banker), can be one of the most powerful positions in government? The Federal Reserve banks are not government entities. They are privately, rather than publicly, owned. How can the president of the New York Fed even be "in government" when he is neither an elected official or even a government employee? And nobody in the "FED" is elected by the people. Nobody at the Fed is answerable to either the people or to Congress, which constitutionally has the exclusive right and duty to "coin money and regulate the value thereof." The Federal Reserve, which is effectively an unconstitutional fourth branch of government, has never even been subjected to an audit. The Federal Reserve Act, was and "Act" (a statutory law), and not a constitutional amendment. And the Act itself was arguably unconstitutional, since the Constitution does not give Congress the authority to delegate its constitutional powers to private parties (even if they have the word "federal" attached to them). And it goes without saying that the right and duty of providing the people with a national currency – honest money – is perhaps the most important, even sacred, single function of Congress or any sovereign government. Chances are, President Obama has never even thought to take a critical look at the Federal Reserve and our debt monetary system. He certainly has yet to say anything which would hint that it is part of our economic problem. He apparently takes it for granted that Federal Reserve Notes are the only kind of money possible, and the Federal Reserve indispensable. So far, it appears the matter of the nature of our money – the most important matter of our times – has not come up for discussion. To quote Richard C. Cook, "Because we are never taught about alternative economic structures, we take this system for granted, though earlier generations had profound fears of becoming what President Martin Van Buren prophetically called a 'bank-ridden society'.” (http://www.globalresearch.ca/...5494 and http://www.globalresearch.ca/..5615) A hundred years ago things were not like this. Both the public and Congress were much more knowledgeable about money matters than they are today, and monetary policy was rigorously debated in both Houses of Congress. In the early 1870s the bankers and their friends were using their influence to both discredit and destroy the Lincoln greenback. They were urging Congress to have the Treasury call in all United States Notes (greenbacks), and do away with them entirely, so that only National Banking note currency would remain in circulation. And they wanted the United States to adopt the gold standard. Most Americans wanted greenbacks to flow freely again, and responsible populist politicians like William Jennings Bryan, wanted a silver standard rather than a gold standard. The reasons were that the American people remembered that greenbacks had helped them prosper during and following the Civil War. When, at the insistence of banking interests, greenbacks were being recalled and taken out of circulation, they felt the squeeze of deflation and fell on harder times. Silver was favored as a basis for our money for a very good reason. We had plenty of it – and were producing more all the time – whereas most of the gold had left the country and was sitting in European bank vaults. In the end, the people won a small victory, and the bankers won another big one in the Resumption Act of 1878. The United States went onto the gold standard, but the greenback receive a renewed, but limited, lease on life. But bank notes would make up the great bulk of our circulating paper. The amount of greenbacks in circulation was thereafter limited to about $350 million. And even those would be redeemable in gold. So, while Americans got to keep their beloved greenbacks, they got nailed onto that proverbial "cross of gold."

We were nailed to that cross when the Federal Reserve Act was passed, to produce an "elastic currency." And we were nailed to it throughout the Great Depression and beyond. That's why FDR could not spend enough to "prime the pump" and get the economy perking again. Money was too expensive! So the richest, most productive nation in the world was crippled. (How can you have an elastic currency and a gold standard at the same time? Obviously, you can't. It didn't work and gold finally had to go.)

Thanks to the elasticity of Federal Reserve currency, the dollar has lost about 98% of its purchasing power since 1913. More than just elastic, it has become downright slimy in nature. Sometimes it's more like silly putty in the hands of shrewd bankers. And, thus, the cross to which we are nailed has gone from one of gold to one of pure and perpetual debt. Lots of it! John Q. Pridger WHERE IS ALL THE GOLD? If we wanted to go onto a gold standard, we'd have to have an awful lot of gold. According to http://en.wikipedia.org:

According to this source, the total "official" gold holdings in September of 2008, was 29,783.9 tons. Of this, the largest single holder of gold was the Eurozone (including the European Central Bank), with 10,911.4 tons. The United States is at the top of individual nations, owning 8,133.5 tons of gold. Germany is second, with 3,413.1 tons. The International Monetary Fund has the third largest gold hoard, at 3,217.3 tons. Ironically – or at least surprisingly – the International Monetary Fund still uses $42.00 per ounce for accounting purposes.

The fact that it is unclear who actually owns the gold held by the IMF, also begs the question as to whether it is clear who actually owns title to the gold reserve "owned" by the United States. Many question whether our gold at Fort Knox (if it is still there), actually belongs to the U.S. Treasury (i.e., the people of the United States), or does it, any percentage of it, belong to the Federal Reserve System banks? The gold is allegedly still there, but we don't really seem to know who holds actual title, since nobody seems inclined to tell us.

IS A RETURN TO A 100% GOLD STANDARD FEASIBLE? If we have over 8,133 tons in gold, and only 4,603 are held at Fort Knox, where is the rest of the gold? But, assuming we do have 8,133.5 tons of gold (and it actually belongs to the American people), would that be enough to back the currency in a nation such as ours? Let's try some calculations. There are 29,166.666 troy ounces in one U.S. ton (2,000 lbs.), so there are 237,227,077.9 ounces of gold in the U.S. gold reserve (29,166.666 X 8,133.5). At a fairly current gold market price of $900 per ounce, we'd only have enough gold to back $213,504,370,100.00 ($213 Billion), in currency. With a GDP of about $14,561,000,000,000.00 ($14.6 Trillion), it would seem we'd come up against a great cash shortage very quickly if we went to a 100% gold back currency. To look at it another way, we only have .79 ounces of gold per capita, considering a population of 300 million – or $711.68 in cash for every man, woman, and child in the nation (at a gold price of $900 an ounce). In other words, it would appear to be impossible, to go to a 100% gold backed national currency without buying an awful lot more gold. And if we have to buy gold at $900.00 an ounce, today, and maybe $2,000.00 an ounce tomorrow, what do we use for money with which to buy it? Or do we just borrow it from somebody? There isn't enough above ground gold in the entire world to back our (or a global) currency in the amounts we need for circulation. Of course, we might be able to do it, at least temporarily, if we valued today's $900 gold at $10,000.00 an ounce. But with all the available gold taken up as currency, the market value of would soon surpass the pegged value anyway, as it always does. In other worlds any gold standard would either be impossible to maintain, or it would have to be based on a fractional reserve system, i.e., a dishonest monetary system. This is why Pridger favors a national fiat (greenback) money system, with token coin, such as we already have, with non-dollar denominated gold and silver coin (both government and privately minted), freely circulating on a free market basis. The gold and silver coin (and bullion) would be legal, bankable, tender at current market rates with regard to the fiat currency. Along with this would be a 100% reserve requirement for current accounts in savings banks. Every nation, of course, would have its own carefully regulated "national currency" strictly for domestic use (which has always been the case). The European Community could keep its Euro if that be the consensus. International money would consist of gold and silver coin and bullion, or gold and silver "travelers' checks." International trade balance of payments would be handled in gold or silver, or under some other universally acceptable international currency, be it Special Drawing Rights (SDR) Certificates or tally sticks. John Q. Pridger Saturday, 24 January, 2009 OBAMA SHOULD USE GREENBACKS TO SAVE THE UNION AGAIN! President Lincoln saved the Union with the issue of greenbacks during the Civil War, and Obama could save the Union again with the same tool. So far President Obama has been totally silent on the most important economic issue of our time – that of the necessity for serious monetary reform. A resurrection of the greenback could deliver us from the financial mess we're presently in. It could be done by taking the privilege of money issue from the private central banking cartel and returning it to the representatives of the people where it rightly belongs. There has never been either a great opportunity, nor imperative, to do it than now. The bankers, and the money power itself, have never been so discredited and vulnerable as they are right now. Now we can truly say that they've had their chance, and they blew it. They have delivered up the whirl wind. The bankers made their big coups in 1863 with the National Banking Act, and in 1913 with the Federal Reserve Act, their greatest bonanza. (145 years of National bank currency and 95 years of Federal Reserve currency.) But the deceptive banking money schemes have finally played themselves out and it's now possible to call their hand. The greenback "legal tender" Acts should not be confused with the National Banking Acts of the same period. The legal tender laws gave us a "national currency" (greenbacks), administered by the government through the Treasury Department. The greenback was subject to Congressional oversight. The greenback was a paper dollar which belonged to the people. The National Banking Acts gave a co-monetary franchise to private bankers. National Bank Notes, also given legal tender status, were banker notes similar to our present Federal Reserve Notes. There remains a lot of public confusion on monetary matters. The most divisive issue with regard to our currency in the period between the Civil War era and 1971 was the matter of the attempt to maintain a gold standard. Since 1971 this is no longer an issue. Our present currency is strictly fiat paper and token coin. Here is a comparison of the costs of bailing out the American economy with our two optional currencies, Federal Reserve money and United States Notes (if we can bring them back into play). Let's look at an even trillion dollar bailout – the cost in Federal Reserve money and greenbacks:

It sounds too simple to be true, of course – that there could be such a convenient option available. But that's how simple it is in principle, and the option is as real as the Legal Tender Laws passed during the Civil War. Due to fractional reserve banking, many times more currency and bank ledger entries will come into existence in the case of FRNs, further expanding the debt (public and private) in an exponential manner, all of which is in the form of bank credits (loans), i.e., debt. Fractional reserve banking would be ended in an honest fiat monetary system. The money in existence would simply remain in existence, and scientifically expanded according to increase in population, the industrial state of the arts, and goods and services available in the national marketplace. The Federal Reserve System is a "trickle down" system. Money originates with the banks of issue (Federal Reserve), and they begin to collect interest on it before it begins to trickle down – first into banks and the financial markets, and then eventually into the real economy. The greenback is a democratic currency. It is spent directly into the real economy from the onset, and serves the people first and foremost. Banks would still have a function – the very function that most people have always assumed they had, but they could no longer create money out of thin air as they can under the fractional reserve system. Money in circulation would be self-limiting, demanding responsible banking procedures and honest and sound lending practices. With an honest money system, there would be no artificial financial or stock market bubbles, and no banking induced boom and bust cycles. Initially, greenbacks would not only be spent into the real economy, but spent to retire the national debt, canceling out Federal Reserve Notes and the debts they represent. This would insure that there would be a sufficient initial issue. The inflationary effects of having so much "cash" in the economy will be neutral, as it would merely replace already existing money with another, and excesses would largely be absorbed as all banks move toward a 100% cash reserve requirement. The Federal Reserve System would either be abolished outright after a transition period, or absorbed into the Treasury as a truly "federal" monetary management branch of government. Here are two currently proposed Monetary Reform Bills which call for a return to greenbacks (United States Notes). One from the The Money Masters.com and the other from the American Monetary Institute. http://www.themoneymasters.com/mra.htm (Monetary Reform Act) http://www.monetary.org/American_Monetary_Act (American Monetary Act) John Q. Pridger THE QUESTION OF THE GOLD STANDARD The Ludwig von Mises Institute and Austrian School of economists favor a return to a species (gold or silver), monetary standard. Pridger personally (along with a lot of others, including the two organizations linked above), see serious problems with the gold standard. The constitutional issue – that only gold or silver can constitute money – is a mute one. The Constitution is silent on the matter. In any case, our government busted out of its "constitutional bounds" a long, long, time ago – since before the Civil War. When the federal government and its "constitutional" activities were small, it was possible to fund its activities with gold and silver coin taxed from trade and various other means. Money was not then something the government had to "create." It was possible that "natural money" could serve the array of needs of both commerce and government. When the Republic was young, mostly foreign coin circulated, and it was possible that the Treasury could produce sufficient coinage through the free minting of gold and silver tendered by private sources or collected through tariffs and taxes. The government did not initially "own" the money that it used and minted. Gold and silver coin were (and continue to be), "natural money" – universally recognized. The only way the government could get ownership of any money at all was through tariffs and other taxation. It could not create or make it. This system was workable as long as government was constitutionally small, and we had a largely agrarian economy. But the growth of the nation, along with the growth of industry and the government itself, dictated that paper (at that time bank paper), for purposes of easy exchange, became a necessary convenience. Naturally, in time, paper, supposedly representing gold or silver, far outpaced the actual gold and silver held in banks. Coin was still king, but paper became an acceptable and necessary substitute, purporting to represent gold and silver. Since banks held most of the gold and silver coin, and issued circulating bank notes representing that coin – stretching the paper money supply through fractional reserve banking – banks (particularly the European banks), were able to maintain a "natural monopoly" on the issue of coin, currency, and credit. A new reality imposed itself with the advent of the Civil War. That war, of course, was itself unconstitutional. It's purpose was to deny the Confederate States the right of self-determination which the British American colonies had declared for themselves (and all peoples), with the Declaration of Independence. The Civil War itself was prompted by European bankers eager to see the United States fail and break up into weaker blocks, more malleable to the money powers of Europe (principally the Bank of England). But with the reality of that war, for better or worse, whether constitutional or not, the necessity of breaking the bankers' money monopoly became apparent. The government had no gold, but needed lots of money with which to execute the war. As a result, the sovereign utility of a scientifically created paper currency became not only apparent, but a dire necessity. The government realized that if it could not "create" its own medium of exchange, it was not really sovereign – it was a vassal of foreign banking powers. The time had come for an honest "national" fiat currency, used for domestic exchange, independent of both foreign and domestic bankers and financiers. The nation was broke in terms of gold, but otherwise very rich and productive. Had Lincoln allowed that only gold and silver could be "constitutional" money, our nation would have once again become a total economic vassal of the mother country. We would have been nailed to the figurative "cross of gold" of which William Jennings Bryant later so eloquently spoke. With the issue of greenbacks, Lincoln was shrewd enough to at least partially avoid the trap of dependence on foreign bankers and their gold "credits" and usurious interest. Though greenbacks saved the Union, the bankers actually finally won the monetary war. For over another hundred years we were nailed to the bankers' cross of gold. Though the gold standard was largely fiction, bankers maintained that fiction with a tight grip on the nation's money supply and credit. The greenback, though it had done its job, and remained in downgraded existence, was thereafter undermined. When the gold standard was finally abandoned, the bankers and their money issuing monopoly were long and firmly established by law, and they have continued as our monetary masters and credit regulators. The Federal Reserve banking System remained our monetary master even though all of our currency had become fiat, bank note, currency. But we remained nailed to that cross just as if their money and bank credits were still good as gold. At this stage, we cannot return to gold and silver as our only "constitutional" money. It never was our only constitutional money. Gold and silver were our "money" only because they had traditionally been universally recognized as "real money" – and the Bank of England insisted on it. "Constitutional" money, however, is what necessity dictates would serve the public good – not what the bankers would dictate, or what "tradition" molded by them dictate. Gold won't work now any better than it has in the past. Three main reasons:

In short, the gold standard was always one of the major bludgeons of the international bankers – the one by which they, for centuries, had held the people and their governments in perpetual debt bondage. While gold advocates are always pointing out (incorrectly), that there has never been a successful fiat money system, we can point out that there has never been a real successful strict gold standard. The gold standard that we had in the United States was a fractional standard, and thus largely fictitious throughout its existence. Our gold standard dollars were in fact just another form of "fiat" currency, falsely claiming to be worth so much in gold. Even actual coin was "fiat" in that it was stated at a fixed amount of value, when in fact, the gold or silver value of coins seldom came close to the alleged value of the coin and paper currency that supposedly represented it. Gold and silver values, vis a vis "money" have always been "fixed" by fiat of government. BUT GOLD AND SILVER NONETHELESS REMAIN "REAL MONEY" There's no doubt that gold and silver coin make the best "store of wealth" monetary instruments. They are hard money, which hold value in everybody's eyes. But what we need is a "currency" that can satisfy all the needs of commerce in modern societies and huge national economies. But governments and economies would be so hamstrung by a strict gold or silver monetary standard that they could not function. The real wealth of a nation is not contingent on the amount of gold and silver in vaults or even the pockets of the people. Wealth comes from the soil and the products of labor, totally independent of gold and silver. What if there were no gold and silver to use for exchange? Nothing would change if there was a viable currency standing in their stead. Gold and silver are not necessary for exchange. "Currency" – a universally accepted medium of exchange – is all that is necessary. A paper ticket will get you into the theater, and a greenback dollar (a universal ticket), will purchase the theater ticket or a dollar's worth of groceries. Federal Reserve Notes do the same thing, but we still owe for each one of them, plus more in interest. By all means, gold and silver should have a monetary role, both domestic and international. Coin should circulate freely on a free market basis. Gold and silver coin should be given "legal tender" status, but be once and for all divorced from a fixed value in terms of circulating paper currency. Gold and silver coin, having monetary (or commodity), value in its own right, should circulate freely, as both government and privately minted coin. Gold and silver are still "real money" by any measure. A gold or silver coin saved is secure value saved. For this reason, precious coins should be bankable too, alongside fiat paper currency, in banks. The preeminent purpose of a national fiat paper currency is to remain in constant circulation, satisfying the everyday needs of domestic commerce. We don't need precious metals for this purpose, but we should retain them for their real value. Precious metal coins in private circulation would also act as a kind of natural regulator, serving as a running comparative check, on and against the fiat circulating currency, helping to instill an extra degree of discipline in the fiat currency system regulating system. Naturally, national currencies would be redeemable in gold or silver coin – but on the free market, and only at free market prices, in a truly free domestic market, rather at a fixed comparative value. Precious metal coins should be denominated in weight rather than national currency units such as dollars, pounds, or yen. Naturally their value in terms of national currencies cannot be realistically fixed, due to the inevitable free market laws of supply and demand, as with any other commodity. Naturally, gold and silver would and should continue to be utilized in settling balance of payments demands in international commerce. It would resume it's role as an international money, while well regulated national fiat currencies would satisfy the exchange demands of national markets. Internationally, exchange and balance of payments in trade matters, can be handled through international forums and agreements, but every nation should have it's own exclusive national currency – one which it alone controls so that domestic economies are no longer totally hostage to international banking cartels. Gold and silver certificates, or warehouse receipts, denominated in weight units, would serve for all international travel, similar to "travelers' checks." These would serve as international money, exchangeable for local national currencies at market values in any nation. We need an honest national monetary unit and system. The greenback is the obvious answer for the United States. They saved the Union once, and the can save the nation again. John Q. Pridger Wednesday, 21 January, 2009 JUST IN CASE – REAL OATH TAKEN WITHOUT A BIBLE Whoops, Obama's oath of office was flawed by a minor transposition of a word. So, out of "an abundance of caution" it was re-administered today – in private, in the White House, without the Bible. One wonders if maybe the "So help me God" may have also have been left out. Not that it matters, as far a the Constitution is concerned. One wonders at all the focus on the "constitutionality" of everything that has to do with the election of this president. Our entire federal government has gone so far out into the left and right backfields of unconstitutional activities for so long that all this worry over the constitutionality of the president would seem totally unwarranted. 90% of our government is unconstitutional. In fact, we cannot help but believe that most of our elected officials take their sacred oaths to "protect and defend the Constitution" with their fingers crossed – more or less as a Kol Nidre pledge (that "The vows shall not be reckoned vows; the obligations shall not be obligatory; nor the oaths be oaths.").

This is why there has been a joke going around the Internet for several years now with regard to coming up with a constitution for the new democratic Iraq. "Why don't we just give them ours?" the punch line goes. "It's a perfectly good one, and we don't use it any more." What difference does it make if Barack Obama is a natural born citizen (the courts didn't even want to hear it) – or whether the oath of office was flubbed up? He's the president for better or worse. John Q. Pridger VULNERABLE PRESIDENTS The powers behind the throne love vulnerable presidents. That vulnerability insures the president's loyalty – not to the Constitution or the people, but to the unseen secret rulers. If an elected president is not exactly with the program, or threatens to stray, this vulnerabilities can be exploited. That is how "the anointers" make sure their chosen one will not cross them. If a president crosses certain well defined lines in the sand during his administration, he is subject to foreclosure by "revelation" or threats thereof. If he doesn't knuckle down and tow the line, he is subject to exposure, impeachment, or other types of removal. If Obama tows the line, nothing will seriously threaten his presidency. If not, things will start happening that will bring him back into the fold or destroy his presidency. Bill Clinton made an ideal president. He was vulnerable on several levels. Had the public been advised of just who they had as a presidential candidate, he would not have been elected. But the media protected his image, and made him look good. But then, he and Hillary had an independent streak on certain issues. When they started talking a little too much about Palestinians deserving a State of their own, a convenient scandal broke loose. He was impeached in the House, but then he launched a significant missile and bombing attack on Iraq, and his approval ratings went up. He and Hillary didn't push for justice for the Palestinians very much thereafter, and all was forgiven – and he went on the win re-election in a landslide. McCain was up front about being with the program. Obviously a little too much for his own good. But Obama, with all his vulnerabilities, would do. He was seen as sufficiently vulnerable and pliable to fill the bill, and his extraordinary popularity with the electorate made him the shoe in. Of course, Pridger hopes Obama will surprise everybody and throw the secret rulers for a loop. But this is very unlikely. He is only one man in the midst of vipers. More likely, he will make the ideal president to do the bidding of the powers around and behind him. John Q. Pridger Tuesday, 20 January, 2009 IT'S DONE! FOR BETTER OR WORSE, BARACK HUSSEIN OBAMA IS THE 44TH PRESIDENT! The Inauguration came off without a hitch. Barack is our president. There were no race riots, terrorist attacks, or other disruptions. Homosexuals and the ACLU are probably about the only ones who had, or have, any reason to the attack the proceedings. Though considerably younger, Pridger is a little like the 105 year old African-American woman who attended the inauguration. "I never thought I'd live to see this day," she said. And all troubling incongruities and cabinet appointments aside, we have no choice now but to look to Obama to pilot our nation through the next four years. It is an historical moment, indeed – in many more ways than one. Not only is Obama the first African-American president, but he is also perhaps the most enigmatic, the most incongruous, president ever elected. To mention a few, consider the following:

Pridger knows how white South Africans must have felt when their old system was overturned and Nelson Mandela was elected president. While Obama is not a communist revolutionary, as Mandela had been – and we are not entering upon a new era of black majority rule, as South Africa was – we are nonetheless (through no fault of Obama), entering into uncharted territory. Our future as a nation is no less on the brink of some unknown sort of revolutionary change than South Africa was as it entered into it's post Apartheid era. The changes we will undergo under the Obama administration remain to be seen. Who Obama really is remains to be seen. And even if he is the man for the job, it will also remain to be seen how much constructive change he will be allowed to bring about. That is, what the powers behind the throne – the ones who "selected him" and then made it possible for him to be overwhelmingly elected – dictate. The challenges the nation faces are not only political and ideological, but economic and financial. We will be (or should be) dealing with the very fundaments in these categories. While Obama's words give even the staunchest conservatives among us at least some hope (with many exceptions, of course), the makeup of his cabinet isn't at all reassuring. Will Obama abandon American global Empire, or will he keep the nation committed to "perpetual war for perpetual peace" in a never-ending fight against the abstract concept of "terrorism" at home, in the Middle East, and elsewhere? Will Obama remain committed to "Israel right or wrong," or will he apply the principles of right and justice to all nations without favor? Will Obama's "change" return America to great and independent nation status in a peaceful world, or merely rearrange the deck chairs on the Titanic? Will Obama's be a truly "American" administration, or will it be dedicated salvaging the New World Order (the wrong New World Order), and the Global Village, with its mega-systems of central banking and financial, and corporate control? Will he champion American values or fall into lockstep with the existing forces of international corporate fascism forging a New World Order? We do not know any of these things yet, since we yet don't really know who Obama is. The electorate was forced to take an awful lot on faith – faith in the image that Barack, with the help of the media, so skillfully presented. In the final election, he was the only candidate that did not blatantly stand for more of the same failed policies. All we can do is hope President Obama turns out to be the right man for the job, and wish him success in bringing about positive change. He'll need not only a lot of luck, but (if he is on the right track), he will also need our help. John Q. Pridger Saturday, 17 January, 2008 CONGRESS IS HELPLESS TO SAVE THE NATION The nation we once had began it's death final plunge in 1913 with the passage of the Federal Reserve Act. With that act, Congress relinquished one of its most important functions and responsibilities to private bankers – its monetary role. President Woodrow Wilson, who was under the sway of the financial sector, signed the legislation. Before his death, however (or even before he signed it), he realized and acknowledged what he had done.

It has been pointed out that the first two sentences of this oft quoted paragraph cannot be verified. But the following two quotes can be, the second quote being very similar to the one above, without the two leading sentences.

It is interesting to note that Woodrow Wilson's book, The New Freedom, was published in 1913, the very year Congress passed the Federal Reserve Act which Wilson signed into law. This would appear to show that he was already very much aware of what he was doing. Either he thought he had thwarted the Money Power with the Federal Reserve Act he was to sign "as it was written" (as some did), or he was foolish enough not to recognize it for what it was. Either that, or he intentionally betrayed his own conscience and inclinations (for which there is some evidence). Nobel Prize winning Milton Friedman is recognized as one of the greatest economists of the twentieth century. While Pridger differs with him on his stand in favor of "free trade" and libertarian brand of internationalism, it should be recognized that Friedman did not think we should have the Federal Reserve, and he was a monetarist, who believed we should use national interest free money, spent into circulation by the government. But he didn't spend much time promoting the greenback (United_States_Notes). It is a great irony that John_Maynard_Keynes' advocacy of deficit spending (spending our way out of economic problems), was tied to the English (and American, under the Federal Reserve) debt money system – the very sort of a system whereby such spending is so dangerous and ultimately destructive. Had we gone to a greenback system of national, interest free, money at the time Nixon slammed the gold window, his statement that "We are all Keynesians now" would not have embodied a national sentence of self destruction as it did. Inflation, maybe, but only as the result of mismanagement of the money supply. Equally ironically, it was at the very time that it was becoming apparent that we would have to abandon the international gold standard that the greenback was seeing its last days. If we were to have a purely fiat currency, interest free United States Notes, rather than debt laden Federal Reserve Notes, should have been the way to go. Had we been on a greenback standard these past forty years, we would not have accumulated the huge national debt that we have. Our money, whether well or poorly managed, would at least have been our own. This huge and critical "mistake" was not an accident, of course. Our monetary policy was in the hands of the bankers' monopoly that profited from it, rather than Congress. In the nearly hundred years since monetary policy issues were last seriously debated around the country and in Congress, Congress had forgot' what monetary policy are. It thinks monetary policy is something only bankers can debate. Our Washington brain trust is literally afraid to bring the issue up. Such things are best left to the Fed central bankers and the international bankers. One of the reasons our politicians are afraid to take up the matter of the nature of money, and reclaim their Constitutional prerogative, "To coin Money, regulate the Value thereof, and of foreign Coin..." is because it would expose the greatest fraud that has ever been perpetrated against a nation of people. A fraud that has gone on for almost a hundred years is pretty hard to explain. And another thing all our elected representatives are afraid of is that this would risk exposing the infamous "international bankers" – the least criticism of whom is now taken to be evidence of the unforgivable sin of anti-Semitism. Whether the international bankers are still predominately "Jewish" bankers or not is really immaterial, the threat nonetheless remains, and it remains for a reason. The Money Power (Jewish and/or Gentile), deems itself "untouchable" and simply doesn't intend to give up its historically entrenched "right" to issue and profit from the money we are obliged to use. The Money Power wasn't quite as entrenched in Lincoln's day as it is now. Thus when Lincoln was faced with having to pump money into to enterprise of saving the Union, he was able to get away with spending greenbacks, made "legal tender" by Congress. He stirred up a hornets nest, of course, but he was able to get the job done. Barack Obama has an excellent opportunity to do today, to save the American economy (and perhaps the Union itself again), by utilizing the tool that Lincoln, the great emancipator, bequeathed to the nation. If it could be done in Lincoln's day, it can be done again. Today the central bankers have been exposed for what they have done, so their position is much weakened, if only the president and the people can be educated fast enough to seize the initiative.